This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

A Senate committee in the Washington state legislature has advanced a medical debt collection bill that could significantly change how medical debt is reported and enforced.

Bob Ferguson yesterday signed a medical debt credit reporting bill into law. Senate Bill 5480 officially prohibits the reporting of medical debt to consumercredit agencies. 🧠 Whats new: The new law will take effect on July 27, and mirrors a now-paused federal rule from the Consumer Financial Protection Bureau.

Appeals Court Reverses Arbitration Ruling for Defendant in Collection Case A New Jersey Appeals Court has overturned a lower courts ruling in favor of a defendant that had granted arbitration in a collection lawsuit more than a year after the complaint had been filed and litigated. More details here. More details here.

A collections notice shows up, a debt collector starts calling or you find a negative report on your credit history, but you know you paid the account in question. Can you sue a company for sending you to collections for money you didn’t owe? How Does the Law Protect Your Rights Regarding CreditCollections and Reporting?

For example, in the US, 92 percent of consumers have cell phones, but just 5 percent of consumers have telco data reported in their traditional creditbureau files. Figure 1: Creditbureau coverage is greater for some types of data than others. FICO has a solution to this problem. market. .

BNPL loans are cited as a potential driver of greater financial inclusion, both in terms of consumer access to the BNPL loan themselves, as well as access to credit products that could enable unbanked and underbanked consumers to establish (or re-establish) their credit histories with one or more of the Consumer Reporting Agencies (CRAs). .

Plus, FICO Score 10 T utilizes a consistent odds-to-score relationship as the prior FICO Score version used by the Enterprises, offering continuity and stability for lenders, investors and consumers. FICO® Score 10 T incorporates trended creditbureau data. FICO Score 10 Suite Available from All Three CreditBureaus.

As the independent standard in credit scoring, FICO® Scores are the leading credit scores used extensively across the lending ecosystem ranging from originations, underwriting and account management to collections and asset-backed securitization. consumer reporting agencies (CRAs). in April 2022. Ethan has a B.S.

One of the primary goals of VantageScore is to provide a model that is used the same way by all three creditbureaus. That would limit some of the disparity between your three major credit scores. So, what are the differences between an Experian credit score calculated using VantageScore and one calculated via the FICO model?

For example, in the US, 92 percent of consumers have cell phones, but just 5 percent of consumers have telco data reported in their traditional creditbureau files. Figure 1: Creditbureau coverage is greater for some types of data than others. FICO has a solution to this problem. market. .

Across EMEA, most countries have now moved past the peaks of the COVID-19 driven lockdowns and restrictions, but the challenges of debt collection in the pandemic remain. There are other factors that will now further stress consumers, including the effect of sanctions from the current crisis in the Ukraine. .

consumer data not present in the traditional creditbureau files) to enhance the predictiveness and inclusiveness in credit scoring. This is especially critical for the approximately 50 million consumers in the U.S. More than 200 million U.S.

To further enhance flexibility and predictive power, the addition of FICO® Score 10 T incorporates trended creditbureau data. FICO® Score 10 and 10 T provide a precise assessment of consumercredit risk on all credit product lines, including mortgages, auto loans, credit cards and personal loans.

FICO® Score At 716, Indicating Improvement In ConsumerCredit Behaviors Despite Pandemic. Ethan Dornhelm wrote: The FICO® Score is the lingua franca, or common language, for the credit scoring industry. It serves as a broad-based, independent standard measure of credit risk. Fewer consumers are actively seeking credit.

Saxon Shirley Fri, 05/20/2022 - 06:06 by FICO expand_less Back To Top Tue, 02/07/2023 - 19:10 As the independent standard in credit scoring, FICO® Scores are the leading credit scores used extensively across the lending ecosystem. million previously “unscorable” consumer files. Read the full post 3. Read the full post 4.

Allowing consumers to demonstrate their regular rent payments will provide a proven indicator of positive financial behavior and will be a useful complement to the FICO ® Score in mortgage lending. There are 53 million consumers who don’t have sufficient data in the traditional creditbureau files to generate a credit score today.

Renting a home, apartment or town house can affect your credit in a number of ways. It’s increasingly common for credit reporting agencies to include positive rental history in consumercredit reports. Having good credit can help you rent an apartment, and paying rent on time can help you build good credit.

And while some of our clients’ business lines benefit from the very latest innovations, others such as mortgage continue to find that older versions of the FICO® Score – even some that were first developed decades ago – meet their needs for credit risk assessment. We also recognize that our scores serve many different purposes.

Credit Risk and FICO Score Trends? And that’s because it generally takes a few months for the effects of that event and the accompanying financial strain to start to show up in consumers’ credit reports, such as in the form of rising balances, credit seeking behavior, and eventually for some, missed payments.

In fact, while other credit scoring models may generate a credit score based on stale credit information , our minimum scoring criteria requires that at least one credit account has updated information reported in the last six months. How frequently the data is updated depends on where it resides: CreditBureau Data.

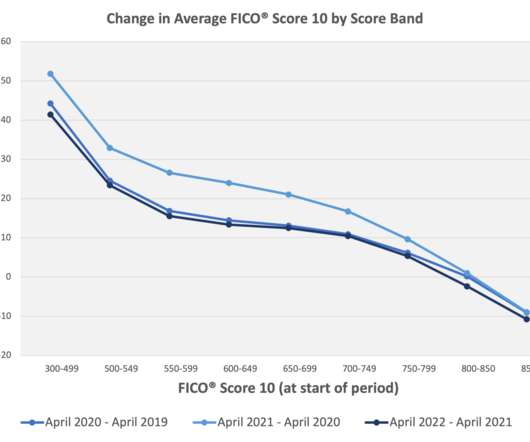

Information and data continue to be key tools at our disposal to better understand the dynamics of the last couple of years, and better navigate what lies ahead for the Canadian consumercredit environment. Comparing Canadian creditbureau data between April 2021 to April 2020, we saw a notable decrease in missed payments.

On March 23, the CFPB released two reports, New Data on the Characteristics of Mortgage Borrowers During the COVID-19 Pandemic and Emergency Savings and Financial Security : Insights from the Making Ends Meet Survey and ConsumerCredit Panel.

Here are some other establishments that CBNA could stand for: CreditBureau of North America: The CreditBureau of North America is a collection agency that collects unpaid debts on behalf of third-party companies. You will likely receive calls and letters from them if this is the case. Conclusion.

Today’s prescreening solutions are very manual in nature, typically involving a list processing agreement with a creditbureau. The solution integrates Equifax ConsumerCredit Information and FICO risk decision management technology with marketing campaign automation and execution.

Today’s prescreening solutions are very manual in nature, typically involving a list processing agreement with a creditbureau. The solution integrates Equifax ConsumerCredit Information and FICO risk decision management technology with marketing campaign automation and execution.

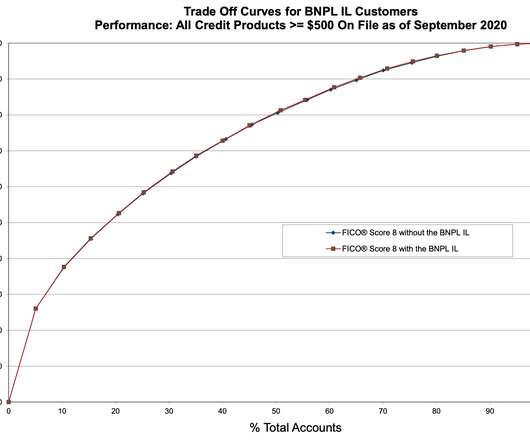

Key findings from FICO research on consumercredit files with recently opened Buy Now, Pay Later loans. market: BNPL reporting approach: How a BNPL lender reports these accounts to a creditbureau can materially influence the impact these loans ultimately have on the FICO® Score. consumercredit files.

Over the past several years, we’ve helped lenders develop on-ramps to mainstream credit using alternative data for those seeking financial inclusion. Our research finds that alternative data sources that demonstrate a consumer’s ability to manage their finances are predictive of consumercredit risk.

Personal loans and credit card debt reached record levels in 2022 due to financial pressures brought on by high inflation and climbing interest rates, according to third-quarter data from a consumercredit reporting agency. These credit market forecasts for consumers exist while 8 in 10 Americans also believe the U.S.

The CFPB said it was concerned about accumulating debt, regulatory arbitrage and data harvesting in a consumercredit market already quickly changing with technology, as GOBaningRates previously reported. The post Equifax, Experian & TransUnion Want to Add BNPL to Credit Reports appeared first on Collection Industry News.

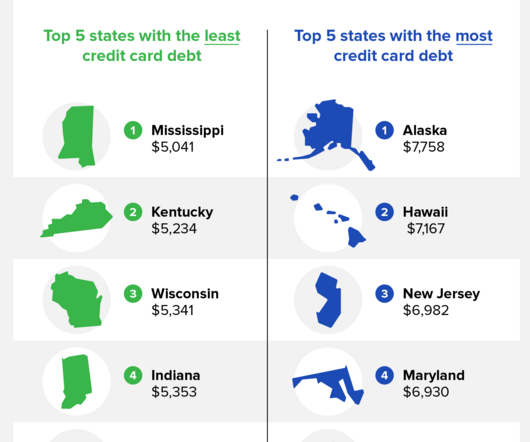

Despite the national average of Americans having over $9,000 in credit card debt per household, only 14% say they’re “very worried” about their debt. 67% of respondents said they have less than $2,000 in debt, which may indicate that only a concentrated number of people have high amounts of credit card debt. Virginia $7,174 6.

A Pre-Screen Firm Offer of Credit, often referred to as pre-approved credit, is a marketing strategy employed by creditors to identify potential customers for their financial products. This process involves a preliminary screening of consumercredit reports to determine if individuals meet specific criteria set by the lender.

Despite the national average of Americans having $9,000 in credit card debt per household, only 14 percent say they’re “very worried” about their debt. 67 percent of respondents said they have less than $2,000 in debt, which may indicate the national average means that a concentrated number of people have high amounts of credit card debt.

The FICO Blog posts last year reflected that – we wrote about everything from the impact on collections, proactive lender communications with consumers, issues with fraud, and of course, how FICO® Scores were impacted. We hope that what readers learned helped instill confidence in keeping credit flowing during uncertain times.

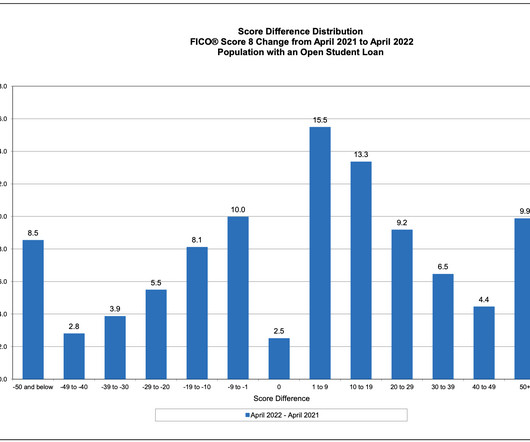

Our analysis looked at depersonalized consumercredit reports from a nationally representative creditbureau sample of consumers who had one or more open student loans as of April 2021 and we observed their credit score change as of April 2022.

From there, you should file a dispute with the creditbureau(s). The Fair Credit Reporting Act requires bureaus to handle disputes with a 30-day investigation. They’re pros at getting inaccurate hard inquires removed from consumercredit reports. Debt collections. Charge offs. Foreclosure.

Easier to qualify for, BNPL has given shoppers, particularly those with little or no credit history, the ability to access – or stack - multiple BNPL arrangements at once without them appearing in bureau data used to assess consumercredit risk. Read Debt Collection and COVID-19: Assessing Affordability.

In addition, given the “variety of sources of information to assess the creditworthiness of prospective borrowers,” the Bureau asserted that “debt collectors may well deceive consumers if they make representations about the nature or extent of improved creditworthiness that result from paying debts in collection.”

Developed by FICO in partnership with LexisNexis Risk Solutions and Equifax, this innovative score utilizes alternative data—data not included in the traditional creditbureau file. The inclusion of this alternative data leads to a more reliable estimate of consumercredit risk and helps score more than 26.5

A collection account will lower your credit score and can generally stay on your credit report for up to seven years. Often, a collection entry will even keep you from getting a mortgage or securing an auto loan, which is why it’s important to do all you can to remove collections from your credit report quickly.

A good credit repair agency should start out by determining exactly which items they can help you with. Doing this typically requires a copy of a credit report from each creditbureau — TransUnion, Experian, and Equifax. What can credit repair companies not do? This isn’t true.

The three major credit bureausTransUnion, Equifax and Experiankeep records regarding peoples credit history. Find out more about what information a creditbureau might have on file for you, how they get it, and how you can see it below. In This Piece What Are the Three CreditBureaus?

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content