This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Bankruptcy can happen to anyone—despite their best efforts. And while most people understand that bankruptcy is generally bad for them, many don’t realize the details of how it can impact you. Read below to find out what happens to your credit score after bankruptcy and what you can do to repair your credit afterward.

When account owners have an account that reflects a negative balance, the lender is faced with a myriad of options and obligations with regard to the pursuit of that debt. Lenders that charge off a debt trigger issuance of the 1099-C when their defined policy leads the lender to discontinue collection activity and discharge a debt.

Here’s what you need to know about getting a new loan and interest rate after bankruptcy. When the Federal Reserve raises interest rates, financialinstitutions increase their rates accordingly, so those with variable interest rate loans may need to pay more interest than when they initially borrowed the money.

When filing for bankruptcy, you can discharge certain types of personal loans, meaning that you’re no longer legally responsible for paying off the debt. If you’re considering filing for bankruptcy, you need to know what personal loans you can discharge and which filing method suits your financial situation.

Incorrect Personal Information Lender Inquiries You Don’t Recognize Accounts You Never Opened Credit Utilization Goes Up Credit Score Goes Up or Down Unexpectedly Public Records You Don’t Recognize. Warning Sign 2: Lender Inquiries You Don’t Recognize. Bankruptcies, for instance, often remain on record for up to a decade.

Meek have been recognized in the January 2022 issue of Lawdragon’ s “500 Leading Bankruptcy & Restructuring Lawyers” List. Lawdragon says, “The start of the pandemic brought expectations for mountains of commercial bankruptcy work. Golden was named in the Bankruptcy & Commercial Litigation specialty.

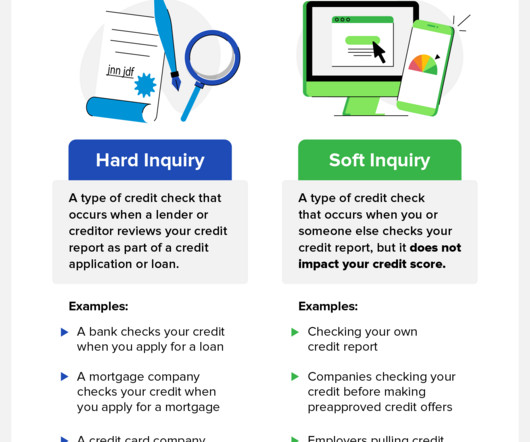

Your credit score is an important aspect of your financial health and is oftentimes used by lenders, landlords, and even employers to determine your creditworthiness. Hard inquiries , also known as hard pulls, are typically made by lenders and other financialinstitutions and can harm your credit score.

When a company files for bankruptcy and it owes you money, it means you have a “claim” in the debtor’s bankruptcy proceedings. The bankruptcy court will establish a deadline, or “bar date,” by which claims must be filed. A claim, in short, is a right to payment. Do You Have to File a Claim? By When Must You File a Claim?

How Does a Bankruptcy Affect my Credit Score? If you’ve been doing a great job making payments on your debts, bankruptcy will have a significant impact on your credit score in the short term. How Long Does Bankruptcy Stay on my Credit Report? Will I be Able to Get Credit After Bankruptcy? Absolutely.

The GLBA Data Protection Law The Gramm-Leach-Bliley Act, or GLBA, is a federal regulation to control how financialinstitutions collect, store, and transmit consumer information. It is not unusual for a company to file bankruptcy after a data breach. Several more states have draft privacy and security laws in draft.

Your credit score is the number that financialinstitutions will use to determine how trustworthy you are as a borrower. That’s why people are sometimes concerned about filing for bankruptcy, as it will reduce their credit score. This is a card that you obtain by giving a down payment to the lender.

SlideBelts is an internet retail company and debtor in bankruptcy. The announced civil settlement resolves claims that the conduct of SlideBelts and its president/CEO violated the False Claims Act and the FinancialInstitutions Reform, Recovery and Enforcement Act (FIRREA). SlideBelts Inc.

This presentation was moderated by the firm’s managing partner, and is geared towards special asset departments of banks and financialinstitutions. The borrower filed for bankruptcy during the foreclosure lawsuit. The lender didn’t recover the full balance of the debt from the foreclosure sale.

COAF is the auto financing arm of the popular financialinstitution Capital One. Hard inquiries allow lenders to access your full credit report from Equifax, Experian, TransUnion, or all three. We’ll also give you a few pointers on getting COAF off your credit report if you didn’t apply for an auto loan with the company.

Both savings accounts and money market accounts are insured by the Federal Deposit Insurance Corporation (FDIC ) with certain financialinstitutions, and in both cases, you generally get instant access to your cash. Lenders scrutinize your credit report—and they look for a good mix of account types.

When youre late on payments or stop making payments on a loan, the lender can repossess or repo the item youre financing to settle your debt. Negotiate with Lender Step 5. When you fail to make payments on time or stop making payments altogether, the lender may demand that you surrender the item. Dispute Inaccuracies Step 4.

FICO® Scores are used by 90% of top lenders ¹Credit score calculated based on FICO® Score 8 model. Your lender or insurer may use a different FICO® Score than FICO® Score 8, or another type of credit score altogether. Late payment may negatively impact your credit score. Results may vary. Learn More $2.50

While you may have applied for a loan from a popular lender or bank, their name isn’t necessarily the one that will appear on your credit report. Instead, banks, lenders, and other financialinstitutions turn to consumer credit reporting companies like CBCInnovis to vet applicants. Ask Lex Law for Help. Charge offs.

Director Chopra discussed potential resolutions on the hypothetical failure of three categories of systemically important financialinstitutions: (1) domestic systemically important financialinstitutions; (2) nonbank systemically important financialinstitutions; and (3) global systemically important banks.

Max has experience representing investment banks, commercial banks, financialinstitutions and other commercial lenders in the origination of debt secured by real estate assets of all types, including office, retail, hotel, apartment, condominium, industrial and self-storage properties.

This section of your credit report tells potential lenders who you are. If you see an old phone number, chances are it is still on file with the financialinstitution that issued the loan or credit card. Soft inquiries occur when you check your own credit score or get a quote from a lender or a pre-approval for a loan.

“Banks, credit unions, and financialinstitutions use credit scores and other factors of your credit history to determine the borrower’s ability to repay the loan,” says David Haas, co-founder of PowerPay , a financial technology company that provides loans for home improvement projects.

“Banks, credit unions, and financialinstitutions use credit scores and other factors of your credit history to determine the borrower’s ability to repay the loan,” says David Haas, co-founder of PowerPay , a financial technology company that provides loans for home improvement projects.

On January 24, the Consumer Financial Protection Bureau (CFPB) proposed a rule that would prohibit covered financialinstitutions from charging fees, such as nonsufficient funds fees, when consumers initiate payment transactions that are instantaneously declined. For more information, click here.

Even in bankruptcy, student loan debt cannot get discharged; it must get paid. No matter what or when, contact your lender if you believe you will be unable to make a student loan debt payment. Lenders are usually very open to figuring out a payment plan. A lower ratio makes a borrower more attractive to a lender.

This would no-doubt portend a new CFPB-styled “Operation Choke Point,” which was the name of the 2013 Department of Justice initiative to investigate financialinstitutions for their role in processing payments to certain categories of lawfully operating merchants that had been associated with high-risk activities. Areas of Practice.

Financialinstitution. When you fail to keep up with payments to a service provider or lender, they often hand your debts off to collections agencies. These agencies might buy your debts for pennies on the dollar or get paid to help the original lender/provider collect. Bankruptcy. Healthcare. Foreclosure.

One of the nation’s premier financialinstitutions, Wells Fargo has over 70 million customers. Whenever you apply for a loan, line of credit, or credit card, the lender or creditor will want to see your credit report to get an idea of how responsibly you’ve used credit in the past. WFDS On My Credit Report. Charge-offs.

The bulletin details recent findings by CFPB examiners that certain loan servicers illegally returned loans to collections after bankruptcy courts discharged the loans. to explain the application of the Fair Housing Act (FHA) and the Equal Credit Opportunity Act (ECOA) to lenders relying on discriminatory home appraisals.

That’s because applying for a credit card, loan, or in this case a Mastercard, often results in banks and lenders checking your credit report. On the other hand, when you complete an application for some form of credit or other financial product, your report may undergo a hard inquiry. eBay Mastercard/SYNCB. Charge offs. Collections.

Common reasons for bank account garnishment in Texas include: Private creditors: These are banks, credit unions, credit card companies, peer-to-peer lenders, hard money loan providers, and other financialinstitutions. This is submitted to the financialinstitution that will remit payment from the debtor’s bank accounts.

Citibank is a major financialinstitution that offers credit cards in partnership with numerous retailers, including: Best Buy. That being said, lenders might be discouraged from approving your application if your credit report is riddled with hard inquiries. NTB/CBNA On My Credit Report. Brooks Brothers. The Home Depot.

The financial pressures have triggered feverish increases in the number of loan impairments for residential and commercial real estate loans. The more impaired a loan becomes, the greater the chance that the borrower will default, causing partial or total losses for the lender. The largest lender in the U.S.,

Much like the Bureau’s recent activity around medical debt , this report seems to signal a wider and more aggressive conversation the CFPB is having with consumers and financialinstitutions about student loan debt.

The bulletin also discusses the “shadow financial” functions enabled by crypto markets, which share many of the vulnerabilities of traditional finance. For more information, click here. In some cases, terms and conditions in nonnegotiable form contracts mislead consumers into believing the terms or conditions are legally enforceable.

According to the FDIC, the entities made misrepresentations about whether they themselves were FDIC-insured and whether the financial products they offered were FDIC-insured. Additionally, the act requires an applicant to submit an affidavit of financial solvency with its application. For more information, click here.

A key development is the growing adoption of Loan Origination Systems (LOS), which have become essential tools for financialinstitutions. The alternative lenders fill a gap left by traditional banks, offering unsecured loans with faster approval processes to individuals who may not qualify for conventional credit.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content