This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The Federal Trade Commission is returning more than $3.7 million to consumers who lost money because of unfair and deceptive loan servicing practices by online lender Avant, LLC. Million To Consumers Harmed by Online Lender Avant appeared first on AccountsRecovery.net.

The Federal Trade Commission yesterday announced a settlement with the owners and operators of a “vast payday lending” scheme that overcharged consumers by millions of dollars which will see all of the outstanding debts be forgiven and deemed paid in full while also banning the defendants from the lending industry.

Lenders and trade groups have criticized the rule for overstepping the original Congressional mandate, and multiple courts have stayed its compliance requirements.

The Consumer Financial Protection Bureau (CFPB)’s decision to establish supervisory powers over nonbank financial institutions will level the playing field and subject those companies to much-needed scrutiny, credit union trade groups informed the agency Tuesday. Response From Credit Union Trade Groups.

The primary aim of an IBR is to provide lenders with an unbiased evaluation of a company’s: Current financial position Future trading prospects Overall business model and financial strategies Management capabilities and operational efficiency Qualified accountants or insolvency practitioners usually carry out IBRs.

A trade group representing non-bank financial institutions that provide sales-based financing to businesses has filed a lawsuit against the Consumer Financial Protection Bureau claiming it has overstepped its authority by issuing a rule regulating how lenders must collect and submit data related to small business lending activities.

Key takeaways: If you are late on car payments, voluntarily returning your vehicle can reduce fees and show responsibility to your lender. Voluntary repossession involves proactively returning a financed car to the lender rather than forcing the lender to seize it back once your loan is in default.

On May 1, 2025, the Federal Trade Commission (FTC)announcedthat it had filed anamended complaintand entered into aproposed final orderwitha debt collector and its owner, resolving allegations that the company engaged in a fraudulent debt collection scheme.

based lender following GAAP accounting, the lender’s net loss rate (or net charge off rate) is the ultimate metric. For lenders, even the largest international banks, loan losses are the largest expense line in the budget so it’s important to prepare for those losses. How do lenders and debt collectors use roll rates?

This code can mean two different things: You don’t have enough accounts for lenders or credit scoring models to effectively gauge your risk as a borrower. Even if you’ve paid your bills on time, if you only have one credit card that’s been open three months, that’s not enough information for many lenders.

Each has its own way of gathering data and scoring your business, but they all look for information from investors, lenders, banks, and credit card issuers. The number of trade experiences is a driving force behind achieving a good business credit score. The way this can backfire is that lenders, in general, frown upon this practice.

But what will that mean for lenders and creditors? since 2020, while open trade lines decreased by 7.7% As consumers battle high inflation and interest rates to afford necessities, budgets will be stretched and many will have to prioritize when and where they spend.

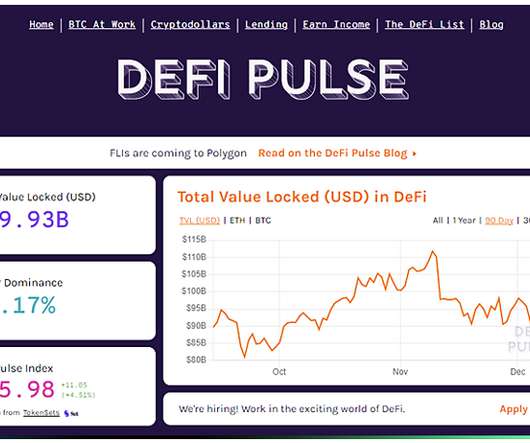

DeFi applications reconstruct traditional finance systems revolving around borrowing, lending, trading, and investing with digital assets. A system that interacts buyers, sellers, borrowers, or lenders with peer-to-peer technology to access financial products or financial services bypassing middlemen such as financial institutions.

On February 11, 2021, the Federal Trade Commission (FTC) announced a $114 million settlement with the owners and operators of an alleged tribal payday lending scheme. Instead, the payday lenders allegedly continued to withdraw funds from consumers’ bank accounts long after their loans had been repaid.

On February 23, the Consumer Financial Protection Bureau (CFPB or Bureau) announced that it has issued orders to nine of the largest auto lenders requesting information about their auto lending portfolios. The Bureau indicated it is interested in the potential correlation between delinquency and geography, credit score, and income.

It marks the highest fine ever issued to a lender for what it deemed a breach of consumer credit rules. As we pass the first anniversary of the pandemic’s outbreak, where does this leave lenders? Right now, we’re advising lenders to adopt a flexible combination of criteria and pre-emptive approaches to evaluate debt risk.

In a major victory for small business lenders, yesterday the U.S. In the event the Supreme Court overturns that Fifth Circuit decision, the CFPB would be required by the Texas federal court’s nationwide injunction to extend every small business lender’s compliance date to compensate for the period stayed. CFPB will dissolve if the U.S.

As result of FTC lawsuit, federal court issues temporary restraining order halting scheme that sent fictitious debt collection notices to consumers nationwide As a result of a Federal Trade Commission lawsuit, a federal court hastemporarily haltedthe operations and frozen the assets of a phantom debt collection scheme and its operators.

On October 27, the Office of the Comptroller of the Currency (OCC) issued its final rule on how to determine when a national bank or federal savings association (referred to collectively as a national bank) is the “true lender” in the context of a partnership between a national bank and a third party.

Since the injunction order was entered, the CFPB has been inundated with requests to extend the stay of the Final Rule to all covered small business lenders. CFPB , finding the CFPB’s funding structure unconstitutional and, therefore, rules promulgated by the Bureau invalid.

The Federal Trade Commission recently extended the deadline , from December 9, 2022, to June 9, 2023, for compliance with the most stringent requirements of its latest rulemaking, revisions to the Safeguards Rule under the Gramm Leach Bliley Act (“the GLBA”).

Depending on the specific credit bureau or bureaus that your vehicle loan lender reports to, it will only show up on those credit reports. There are three different credit bureaus that are mainly used by all lenders: Experian, Equifax, and Transunion. This is crucial in knowing how a new vehicle loan can increase your credit score.

Every lender will have different DTI requirements, but it’s generally recommended to stay below 36%. Gather Proof of Income Potential lenders want to see you have a reliable source of income, especially if your credit score needs some work. Each lender will offer different loan terms.

While creditors weren’t looking up someone’s history of debt and payments, many lenders did take risk-mitigation actions. It also impacted some people’s ability to get credit with new lenders. It became possible for lenders to receive electronic information about a person’s credit quickly in the form of a fax.

Average Car Loans by Age Group Average Car Loan Term by Credit Score Car Loans by Lender Type 4 Tips to Lower Your Car Payments 2023 Car Loan Statistics Key Findings Knowing the different statistics for monthly car payments can help you have a better idea of where you stand before purchasing a vehicle. 781 to 850 61.6 661 to 780 70.15

Those were just two of more than 1,800 loans that went to debt collectors and high-interest lenders through the Paycheck Protection Program, according to an analysis by The Washington Post. Twenty-five have been subject to legal enforcement or consumer alerts, many by the CFPB and the Federal Trade Commission.

The industry trade teams challenging the CFPB’s rule that is final Payday, Vehicle Title, and Certain High-Cost Installment Loans (the Rule) have filed a movement for summary judgment. The post Trade Groups File Summary Judgment Motion In Texas Lawsuit Challenging CFPB Loan Rule That Is Payday appeared first on Collection Industry News.

Job gains showed up in health care, social assistance, transportation and warehousing, along with retail trade, which reflected the return of workers from a strike, while federal government employment declined as a result of wide-reaching layoffs. The Federal Reserve (Fed) held rates steady at 4.25-4.50% 4.50% in March.

Publicly-Traded REITs. These companies trade on public stock exchanges, which makes them extremely liquid. A combined strength and weakness of publicly-traded REITs is their dividend yield. Because they trade on public stock exchanges, they tend to move in disturbing correlation with stock indexes.

The Financial conduct authority has asked banks, lenders and debt collectors for advice on how to deal with the fall out from emergency Covid-19 loans given out during the pandemic. But it will advise banks and lenders on how to manage repayment of loans linked to the COVID-19 crisis without violating consumer rights.

In addition, the research reveals that of those firms who have heard back from their lender about a BBLS or CBILS facility, nine out of ten have had their application approved. The coronavirus crisis has created huge challenges for businesses, and lenders are committed to giving companies of all shapes and sizes the right support.

CFS Associate Addison Morgan represents several of the nation’s preeminent financial institutions in litigation arising under the Fair Credit Reporting Act, Telephone Consumer Protection Act, Fair Debt Collection Practices Act, Federal Trade Commission Holder Rule, and other consumer protection state analogs.

trillion SME funding gap in unmet trade finance, with demand for funding of small businesses rapidly becoming an acute challenge. It’s a mind-boggling number largely driven by demand for unfilled or rejected trade finance applications tabled by small businesses in emerging markets. New Lenders. Technology.

In a recently issued procedural notice , the Small Business Association (“SBA”) addressed a lingering question of borrowers and lenders related to the Paycheck Protection Program (“PPP”) process: What procedures are required for changes of ownership of an entity that has received PPP funds?

The auto loan industry is quite a diverse one, and loan terms can vary considerably from one lender to another. Many lenders will provide 100% financing, but others may require down payment as high as 20% of the value of the vehicle. Auto dealers work very closely with subprime auto lenders. Typical Terms for Car Loans.

Quantuma was appointed by one of the firm’s lenders, Fenchurch Legal, in July. They attended the company’s trading premises and found the site completely cleared of all office equipment and furniture. McDermott Smith, established in February 2016, had one remaining director, founder and solicitor Andrew Smith.

Borrowing money from a bricks-and-mortar bank, an online lender or a peer-to-peer marketplace and then paying it back has become a way of life for most, if not all, Americans. Lenders like Discover or Citibank indicate your credit score on their statements and their online portals provide breakdowns of how your credit score evolves over time.

UK businesses are returning to work this month with some trepidation, according to fintech business lender MarketFinance. This coupled with a very moderate outlook for trading conditions, ‘rent quarter day’ this week and uncertainty about their workforce, no doubt this will put further pressure on businesses.”.

The letter should include details about the debt, the original lender, and the debt collector’s authority to collect the money. If the debt collector continues with attempts to contact you, you can submit a complaint with the CFPB , your state’s attorney general’s office , or the Federal Trade Commission.

It shows lenders that you’re serious about this investment and can make payments on time. The Federal Trade Commission has reported that one in five people have an error on their report. The Federal Trade Commission has reported that one in five people have an error on their report. Lenders want to protect their investments.

For instance, the insolvency practitioner may recommend a Company Voluntary Arrangement (CVA) if the business is able to keep trading while paying back its debts. In summary, when two businesses are involved in an intercompany loan, the lender risks not receiving repayment if the lendee becomes insolvent and ultimately enters liquidation.

When you stop making payments on an auto loan, the lender will take the vehicle back. Your first option is to start negotiating with your original auto lender. This could be a bank, an online lender like Capital One, or the in-house finance company at the dealership. It means your lender has lost money on your loan.

If you’ve gotten behind on payments to a creditor or lender, your debt could be sent to collections after around 120 days of missed payments. Paying off collections can help your credit score if the lender reports to new credit scoring models, including FICO 9®, FICO 10®, VantageScore 3.0® ® and VantageScore 4.0®.

As seen in Figure 2, not only does the FICO® Score suite deliver scores on more consumers, but the consumers we do score (relative to the “Credit Bureau Data Research Score”) are more likely to fall in the “new to credit” and “no credit bureau record/trade” segments. These consumers are stuck in a catch-22.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content