This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The CFDCPA does not apply to anyone who collects their debts or government personnel in the United States. What is Colorado Uniform ConsumerCredit Code (Colorado UCCC). The Uniform ConsumerCredit Code (UCCC) is a Colorado state legislation governing how consumercredit is handled.

The Bank of England Governor also poured cold water on those who might expect growth to be maintained, suggesting that output at the end of Q3 will still be 10% lower than at the end of 2019 ? The true, underlying condition of the economy is clouded by the sheer scale of Government interventions since the start of the pandemic.

Concerningly for lower-income households, organizations distributing federal financial support expect they’ll be able to help roughly one million fewer families pay their energy bills this year, in part due to government funding for the Low Income Home Energy Assistance Program (LIHEAP) falling by $2 billion from last fiscal year.

Bottom line: households took on more debt at the end of last year and we’re seeing loans increasingly going bad, according to data from the Federal Reserve Bank of New York, leading to a shift in consumer spending for 2024.

25% despite concerns around the turmoil that has shaken the banking system , landing it at 4.75-5%. At the beginning of March, the federal government ended pandemic-era payments for low-income families on the Supplemental Nutrition Assistance Program (SNAP), causing nearly 30 million Americans to lose increased food stamp benefits.

Credit card borrowing rose in November to its highest monthly level since 2004 according to latest Bank of England data. billion in all forms of consumercredit, an increase on the £700m borrowed in October, of which £1.2 It is important that everybody accessing the consumercredit sector is exercising best practise.

Each year, we provide insight into the national average FICO® Score to help ensure consumers have a baseline measure of credit health standing. Government stimulus programs have been ramping down and payment accommodations reported in the credit bureau data have largely reverted to their pre-pandemic levels. Average U.S.

The impact of the pandemic on the credit/consumer eco-system has been profound, but the CSA?s s member firms have continued to facilitate payment deferrals and offer forbearance beyond the Government?s s requirements. Collections and recoveries remain an important part of the economic ? s Debt Management function.

To celebrate this important milestone, Troutman Pepper’s Consumer Financial Services Law Monitor would like to dedicate today’s blog to the FCRA. The FCRA regulates the collection, dissemination, and use of consumer information, including consumercredit information. and throughout the world.

On January 20, 2023, California Attorney General Rob Bonta submitted a letter to the CFPB agreeing with its preliminary determination that California’s Commercial Financing Disclosures Law (CFDL) is not preempted by TILA because the CFDL only applies to commercial financing and not to consumercredit transactions within the scope of TILA.

economy, credit scores, and credit risk trends were headed. government and financial institutions to implement significant guard rails and safety net programs for consumers such as the government stimulus, extended unemployment benefits, and payment accommodations. consumers decreased on a year-over-year basis.

Find out more about free credit repair for low-income families and individuals below. Check your financial accounts for any credit reporting perks. Some credit card and banking accounts come with credit reporting perks. A Free Look at Your Credit Score Credit scores and reports aren’t the same thing.

According to the Federal Reserve’s ConsumerCredit report, 43.5 Not only can you not declare bankruptcy on many forms of student loan debt, but it can also harm your credit. Student loan debt by state The Federal Reserve Bank of New York tracks student loan debt by state. Each borrower owes an average of $37,787.

The just recently released Federal Reserve ConsumerCredit-G.19 consumercredit outstanding has reached historic levels; outstanding consumercredit is now at $4.7 In August, consumercredit increased at a seasonally adjusted annual rate of 8.3 19 report shows that U.S.

This settlement is yet another example of an activity that the State Attorneys Generals across the United States view as germane to their mandate to protect consumers, especially from perceived unfair or unlawful consumer lending practices.

The CFPB is concerned about accumulating debt, regulatory arbitrage, and data harvesting in a consumercredit market already quickly changing with technology. Scammers impersonate the government or businesses, which has resulted in $2 billion in losses between October 2020 and September 2021. For more information, click here.

On December 1, the CFPB published research regarding banks and overdraft fees. It found that banks continue to rely heavily on overdraft and non-sufficient funds revenue, which reached an estimated $15.47 On November 8, New York Governor Kathy Hochul signed into law the “ConsumerCredit Fairness Act” (S.153).

Government launches consultation on reform of ConsumerCredit Act. HM Treasury has issued a consultation seeking stakeholder views on reform of the ConsumerCredit Act 1974 (CCA). FCA: Credit Information Market Study: interim report Closing date: 24 February 2023. Consultations.

NEW YORK—The Federal Reserve Bank of New York’s Center for Microeconomic Data today issued its Quarterly Report on Household Debt and Credit . The report is based on data from the New York Fed’s nationally representative ConsumerCredit Panel.

NEW YORK — The Federal Reserve Bank of New York’s Center for Microeconomic Data today issued its Quarterly Report on Household Debt and Credit. The report is based on data from the New York Fed’s nationally representative ConsumerCredit Panel.

René is a banking and regulation professional with a decade of experience and a special interest in risk modeling, measurement and management. Tomas Klinger, decision science and data director at Home Credit (previous winner). From 2007 he has specialized in financial services and consumercredit. by Nikhil Behl.

But the central bank forecast another three-quarter point in rate increases next year, more than it previously estimated. Credit Card, Personal Loan Delinquencies Expected to Surge in 2023. The company’s 2023 ConsumerCredit Forecast released Wednesday projects serious credit card delinquencies will climb to 2.6%

FICO has been the pioneer in incorporating data from outside the credit bureaus, like cash flow data, to obtain a clearer and more accurate picture of consumer financial risk. Among consumers who don’t have enough credit history to generate a traditional FICO Score, over 15 million could receive an UltraFICO Score.

On November 8, while at the Central Bank of Ireland, Federal Reserve Governor Lisa D. On November 8, the European Banking Authority issued draft guidelines defining how stablecoin issuers should structure their risk and management recovery plans concerning reserve assets. For more information, click here.

Credit Counselor. A credit counselor is certified and trained in consumercredit, money and debt management, and budgeting. Garnishment is when a creditor takes part of your paycheck or money from your bank account to collect money you owe on a judgment. Garnishment. Garnishments generally require a court order.

The four key trends we’re studying are: resumed foreclosure activity, extensive medical bills, the end of child tax credits and historically high inflation. Add these all together and the financial outlook for consumers, especially those in debt, is scary. But there are silver linings, as well. And lenders are happy to lend.

Among these are recommendations related to the regulation of non-banks and fintech companies, including: Recommending that Congress either (i) “authorize the Bureau to issue licenses to non-depository institutions that provide lending, money transmission, and payments services,” with licenses “provid[ing] that these institutions are governed by the (..)

The bill requires stablecoins to be backed by government securities with maturities less than 12 months or domestic dollars, while requiring stablecoin issuers to publicly release audited reports of reserves executed by third-party auditors. Bill Hagerty (R-TN), introduced the Stablecoin Transparency Act (S. 3970 and H.R.

This letter follows Chairman Clyburn’s May 2022 letters to the NCRAs, requesting information on the companies’ efforts to respond to and resolve credit reporting inaccuracies raised by consumers during the pandemic. For more information, click here. For more information, click here. For more information, click here. and the U.S.,

This bill would instruct the Consumer Financial Protection Bureau (CFPB) and the Government Accountability Office to conduct a study on BNPL and EWA services to help determine the degree to which consumers are utilizing both services for retail purchases. For more information, click here. For more information, click here.

It marks the highest fine ever issued to a lender for what it deemed a breach of consumercredit rules. But more tellingly, the penalty related to the mistreatment of business and personal customers who fell behind on credit card and loan payments between 2014 and 2018 – well before many of us had even heard of COVID-19.

In May 2020, the FTC charged a payday lending enterprise with deceptively overcharging consumers millions of dollars and withdrawing money repeatedly from consumers’ bank accounts without their permission. For more information, click here. For more information, click here. For more information, click here.

NEW YORK—The Federal Reserve Bank of New York’s Center for Microeconomic Data today issued its Quarterly Report on Household Debt and Credit. The report is based on data from the New York Fed’s nationally representative ConsumerCredit Panel. Credit card accounts expanded by 5.48 quarterly increase. million to 578.35

In uncertain environments, lenders seek ways to address credit risk management gaps likely to emerge with a potential recession. Leveraging FICO® Resilience Index to keep credit flowing. A renewed focus on portfolio resilience is key, especially in the face of economic stress.

In uncertain environments, lenders seek ways to address credit risk management gaps likely to emerge with a potential recession. Leveraging FICO® Resilience Index to keep credit flowing. A renewed focus on portfolio resilience is key, especially in the face of economic stress.

On October 23, lawmakers in the House of Representatives introduced a bill to exclude Paycheck Protection Program (PPP) loans from regulators’ calculations of the asset size of smaller banks. The legislation would benefit banks and credit unions with assets under $15 billion. For more information, click here.

trillion on their credit cards, according to a new report on household debt from the Federal Reserve Bank of New York. Credit card balances spiked by $154 billion year over year, notching the largest increase since 1999, the New York Fed found. Americans now owe $1.08

On October 11, the Consumer Financial Protection Bureau (CFPB) issued an advisory opinion concerning consumers’ requests for information regarding their accounts with large banks and credit unions. For more information, click here. Existing law currently required this disclosure only until January 1, 2024.

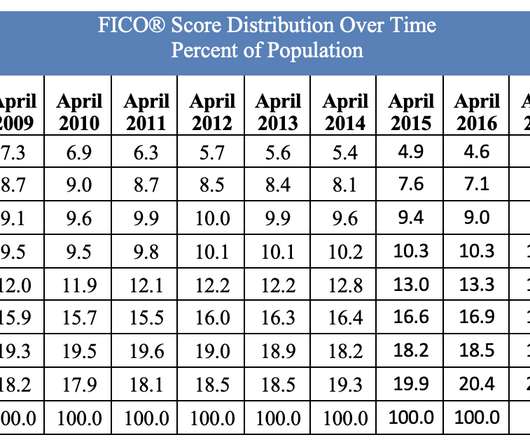

In our top post, Vice President and General Manager of Scores, Sally Taylor explained the new FICO Resilience Index, designed to provide lenders with a more precise assessment of consumercredit risk and consumers with demonstrated talent for weathering economic storms greater access to credit. As of July 2020, just 7.3%

Unemployment rate is typically a key factor used in credit card loss forecasting models due to its high correlation with delinquency and loss. However, unlike during the Great Recession, government stimulus and payment deferral programs kept delinquency at bay when unemployment reached its peak in 2020. bank and credit card industry.

Drawing on expertise from key governmental bodies, the proposed legislation seeks to establish a comprehensive framework for stablecoin governance. Senator Lummis, a vocal supporter of Bitcoin, has been more critical of stablecoins, particularly Tether, and has opposed central bank digital currencies. For more information, click here.

The Taskforce was in part inspired by the National Commission on Consumer Finance, which was established by the ConsumerCredit Protection Act in 1968 to conduct original research and provide recommendations relating to the regulation of consumercredit. To read the Taskforce Report Volume I click here: [link] .

“We did have a crisis,” said Brian Riley, director of credit advisory services at Mercator Advisory Group, “but because of the support that was given, it really kept the market for consumercredit steady.”. He added that card issuers behaved “a lot more rationally” in comparison with the 2007-2009 crisis.

Circuit Court of Appeals ruled that the Fair Credit Reporting Act does not require consumercredit agencies to further investigate when a borrower disputes a debt collector’s ownership of their debt. Attorneys for the borrowers and credit agencies did not immediately reply to requests for comment on Friday. Jody Godoy.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content