This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Chase was one of 13 financialinstitution censured for robo-signing documents in support of debt collection suits and foreclosure. If you are the person at the creditor’s company responsible for signing and or processing these affidavits, please do not just sign them as a matter of course.

At the same time, however, the account owner/debtor is still responsible for the balance, and the lender/creditor can still make an effort to collect what is owed, with obvious exceptions being discharged or dischargeable bankruptcy filings. Charging Off” Uncollectable Debt. 1.6050P-1(b)(2)(i). See IRS Info. 2005–0207, 2005 WL 3561135 (Dec.

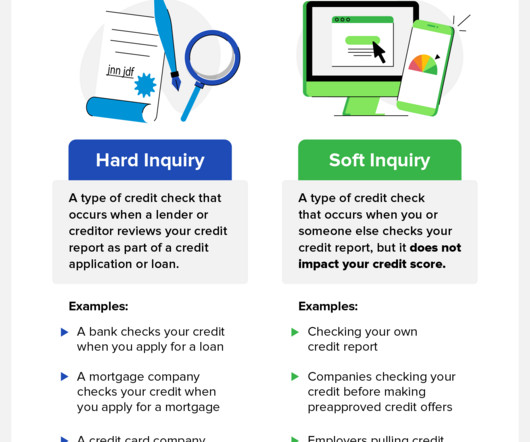

However, if a lender or creditor checks your credit score as part of a credit application or loan, it is considered a “hard inquiry,” which can potentially lower your score by a few points. Hard inquiries , also known as hard pulls, are typically made by lenders and other financialinstitutions and can harm your credit score.

The EU has undertaken several legislative measures to tackle over-indebtedness and provide relief for over-indebted individuals or entities, prioritising negotiated solutions between debtors and creditors, often involving court supervision or approval.

The EU has undertaken several legislative measures to tackle over-indebtedness and provide relief for over-indebted individuals or entities, prioritising negotiated solutions between debtors and creditors, often involving court supervision or approval.

From Burr & Forman’s Greenville office: Rachel Gilbert is a member of the firm’s Health Care Practice Group, focusing on assisting hospital clients with regulatory compliance, transactions, financial strategies, and advocacy related to participation in federal and state reimbursement programs.

When the Federal Reserve raises interest rates, financialinstitutions increase their rates accordingly, so those with variable interest rate loans may need to pay more interest than when they initially borrowed the money. Filing for Chapter 13 bankruptcy is also critically important if you’re at risk of home foreclosure.

A creditor with a claim must often take affirmative action by filing a “proof of claim” form in order to preserve and protect its rights to payment. Even when a claim is scheduled, and assuming there are no reasons not to (see below), a creditor may choose to file a claim to guard against a debtor modifying or removing its scheduled claim.

A recent decision from a Louisiana district court should provide some comfort to banks and other financialinstitutions who acquire other entities by merger – at least in the Fifth Circuit, they are not debt collectors. As most know, Bank of America (BoA) acquired Countrywide Bank FSB and its mortgage portfolio in 2008. In Jackson v.

If you see an old phone number, chances are it is still on file with the financialinstitution that issued the loan or credit card. Your creditors will report on your credit accounts regularly. Account information for each credit item will include the following: Name and address of the creditor. Foreclosure.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. You may access this interactive tool at [link]. According to the FOMC, inflation continues to run below 2%. For more information, click here.

Citibank is a major financialinstitution that offers credit cards in partnership with numerous retailers, including: Best Buy. Hard credit pulls let creditors see your credit reports , giving them an idea of how responsibly you use credit. Foreclosure. NTB/CBNA On My Credit Report. Brooks Brothers. The Home Depot.

NSF fees are distinct from overdraft fees, which financialinstitutions charge when they pay, rather than decline, a payment when the account lacks sufficient funds. On October 11, the CFPB published its analysis regarding the nonsufficient fund (NSF) fee practices of a number of banks and credit unions. On October 10, D.C.

The first of its kind, the strategy examines the phenomenon of financialinstitutions de-risking and its causes, and it identifies those greatest impacted. Department of the Treasury issued the 2023 De-Risking Strategy, as mandated by Congress in the Anti-Money Laundering Act of 2020. For more information, click here.

Attorneys who collect for national banks, debt buyers or other financialinstitutions have been regular targets in FDCPA class actions. 2016) (granting summary judgment for plaintiff in FDCPA class action where defendant’s letter failed to specifically identify the name of the current creditor); Avila v. 3d 317 (7th Cir.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. You may access this interactive tool at [link]. Currently, the act only applies to persons who service student loans.

Financialinstitutions, servicers, lenders, and debt collectors must stay up-to-date on evolving federal and state laws stemming from the COVID-19 pandemic, as such laws impact all facets of consumer loan servicing and debt collection. Colorado – On June 29, 2020, the Colorado legislature enacted Senate Bill 20-211.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. The law does not impact most third-party collection agencies, but it does impact some creditors and debt buyers.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. You may access this interactive tool at [link]. State Activities. Privacy and Cybersecurity Activities.

The rule will be intended to “facilitate enforcement of fair lending laws as well as enable communities, governmental entities, and creditors to identify business and community development needs and opportunities of women-owned, minority-owned, and small businesses.” The Bureau expects to issue this NPRM by September 2021.

On April 26, the CFPB issued an advisory opinion, reminding the industry that a debt collector who brings or threatens to bring a foreclosure action to collect a time-barred mortgage debt may violate the Fair Debt Collection Practices Act. For more information, click here. For more information, click here. For more information, click here.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. You may access this interactive tool at [link]. For more information, click here. For more information, click here.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. You may access this interactive tool at [link]. For more information, click here.

The company expects to have sufficient funds to fully repay unsecured creditors. The bill would ban all medical debt from appearing on credit reports and prohibit creditors from considering medical debt in their decisions on whether to extend them credit. Bittrex had previously paid more than $29 million in fines for alleged U.S.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content