This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Recent regulatory activity makes it clear: regulators care as much about consumer preference in debtcollection as creditors. In this blog post, Kelly Knepper-Stephens, TrueAccord’s VP Legal & Compliance, highlights the recent laws and regulations designed to protect consumer preferences in debtcollection.

Debt collectors are notorious for harassing consumers when they seek repayment, calling excessively and threatening to take actions that may not be legal. What you may not know is that you are protected by the FairDebtCollection Practices Act (FDCPA), a law designed to keep third-party debt collectors in check when they contact you.

Does Colorado Law Protect Me From Debt Collectors? When collecting a debt from you, collection agencies must adhere to federal and state rules. Fortunately, the federal FairDebtCollection Practices Act (FDCPA) protects all states. What is the Federal FairDebtCollection Practices Act (FDCPA)?

How Does the Law Protect Your Rights Regarding Credit Collections and Reporting? Numerous federal and state laws protect your rights to fair and accurate credit reporting. Some of those laws also cover your rights as a consumer to fairdebtcollection practices. How Do You Sue a Collection Agency or Other Creditor?

Your credit score may improve if your collectiondebt is reported to a new credit scoring model—FICO 9®, FICO 10®, VantageScore 3.0® Most creditors still report to old scoring models, so it’s unlikely paying off the debt will improve your credit score. How Does CollectionsDebt Affect Your Credit Score?

Regardless of what a debt collector might tell you, you have a lot of rights when it comes to how debt can be collected. In fact, merely mentioning that you understand your rights will, many times, stop debt collectors in their tracks. Your rights come from the FairDebtCollection Practices Act (FDCPA).

Consumers Prefer Digital DebtCollection By and large, consumers prefer to communicate with their collection agencies digitally—they already predominantly communicate with their banks, creditors, and lenders digitally, so digital collection is a smooth transition when an account moves to collection.

FAQ Consider Hiring a Credit Repair Company How Collection Accounts Impact Your Credit Collection accounts have a significantly damaging impact on your credit score because they’re negative marks that indicate to lenders you may not pay your bills on time—or ever. Does your account information seem accurate?

That increases the likelihood of data being misconstrued and debts being assigned to the incorrect party. You also want to make sure the debt isn’t part of an identity theft issue because you didn’t know about it already. The process may start when you get a phone call from a debt collector.

Fortunately, the knowledgeable team at TrueAccord is here to help break down some of the top questions around compliance in the collections industry. The Questions: What are the major regulations lenders need to know about? What are the top challenges that you see ahead for compliance in collection?

If a debt is 10 years old but you were making payments under an agreement with the lender until 3 years ago, the debt is likely still within the statute of limitations and can be pursued by a debt collector. How Long Can a Debt Collector Pursue an Old Debt? Can a Bill Collector Collect After Seven Years?

Trying to keep up with regulations in debtcollection can feel overwhelming especially with new cases and federal guidance coming out regularly interpreting the law and states actively amending or creating new laws that impact debt collectors, original creditors, and current creditors.

District Court for the District of New Jersey found that the plaintiff had not suffered an injury in fact and therefore lacked standing to assert a claim under the FairDebtCollections Practices Act (FDCPA). The plaintiff incurred a debt to a bank, which sold the account to a new creditor.

With uncertainties about how the end of various pandemic-era benefits will impact consumers, it’s more important than ever for creditors and collectors to implement strategies that consider consumer situations and preferences when attempting to collect. Meet consumers where they are, compliantly.

Portfolio Recovery Associates, LLC, is a collection agency that buys old debts from lenders and companies that have been unable to collect the debt themselves. Portfolio Recovery buys multiple accounts with old debt from companies that have given up and “charged off” the accounts.

If you have been contacted by Sunrise Credit Services, you are probably being pursued for an old debt. Sunrise Credit Services is a debt collector that has been hired by your old creditor to collect payment on your debt. They may also have purchased the debt to profit off your payments.

The result, not surprisingly, is that New York consumers who had already opted in to communicate via email about the account with the creditor would, after falling behind on payments and being referred to a debt collector, only receive phone calls and letters from debt collectors. Comments were due February 13, 2023.

How Long Can a Debt Collector Pursue an Old Debt? Each state has a law referred to as a statute of limitations that spells out the time period during which a creditor or collector may sue borrowers to collectdebts. In most states, they run between four and six years after the last payment was made on the debt.

They also might be charging you the full amount in order to make a profit, since credit collection agencies typically buy collection accounts at a discount from the original lender. Debt Validation. Provided by the FairDebtCollection Practices Act, you have the right to demand debt validation from a collection agency.

The payday lenders like Speedy Cash swear up and down that they don’t have anything to do with this, but somehow their customer lists keep getting into the hands of fraudsters. CREDITOR : SPEEDY CASH SERVICES. We will be forced to proceed legally against you and once it is processed the creditor has entire rights ?

If you send Asset Acceptance a short debt validation letter (using our free template) within 30 days, the agency has to provide you with details about the debt. This should include information like who the original lender or creditor was, how much you owe, and your account number. Failing to validate the debt.

Gavin Newsom recently signed SB 1286 amending the Rosenthal FairDebtCollection Practices Act’s coverage to certain commercial debt. Prior to this amendment, the RFDCPA’s restrictions applied only to certain debt collectors and creditorscollecting consumer debt. California Gov.

Does a judicial foreclosure action constitute “debtcollection activity” under the FairDebtCollection Practices Act (“FDCPA”)? The answer depends on whether the creditor attempts to recover the unpaid mortgage balance or just the property, according to the U.S. Routh Crabtree Olson, P.C.

Has your credit score recently taken a dive as a result of a collections entry from Penn Credit? If you forgot to pay a bill or you’ve gotten behind on payments to a lender or service provider, it can have some nasty effects on your credit. Try out one of the approaches below, and you could be collections-free in a few weeks.

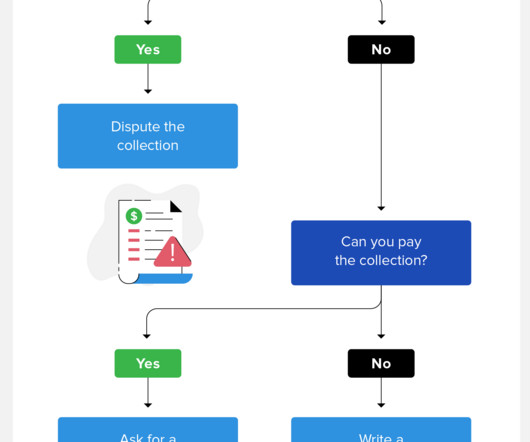

Ask for Proof of the Debt. You could be contacted about a debt you’ve already paid or one that was never yours, to begin with. The FairDebtCollection Practices Act safeguards you here, requiring collections agencies to verify your debt by providing documentation of it before they can collect.

Common examples of consumer debtcollection scenarios might include a credit card company attempting to recover unpaid balances, a hospital seeking repayment for medical bills, or a mortgage lender attempting to recover delinquent mortgage payments.

When you forget to pay a bill on a loan, credit card, or medical debt, and the original lender or provider is unsuccessful at getting you to pay your debt, they turn to debt collectors like RMS. Here are three methods that may work: Ask RMS for proof that the debt is yours. Ask RMS for Proof the Debt is Yours.

Agencies like ARstrat usually get access to you and your debts in one of two ways. They are employed by service providers/lenders to help collect on debts, earning a fee when you make a payment. Before you even think about paying ARstrat, you should ask to see some evidence of the debt they’re seeking payment for.

Conversely, if your business is on the receiving end of this letter, we also discuss the nitty-gritty of the debtcollection letter. The Basics of a DebtCollection Letter. Debtcollection letters can be issued to both commercial and consumer debtors. The Purpose of a DebtCollection Letter.

The creditor referred the account to a law firm, which served the consumer with a collection suit and obtained a default judgment for the balance. The law firm sent four post-judgment collection letters, demanding the $4,225.74 The consumer filed suit against the law firm that sent the collection letters in the U.S.

If you have had a bill go into collections, you may start hearing from a company called Advanced Collection Bureau Inc. They are a debt collector that has either been hired by your original creditor or has purchased the debt at a fraction of the price. What is Advanced Collection Bureau Inc?

Nationwide Recovery Service will appear on your credit report as a collection agency. This is because the original creditor of your debt has hired them to recover payments from you. You may find that the same debt is listed twice: once for the original creditor and once for Nationwide Recovery Service.

From our own experience, many of TrueAccord’s creditor-clients prefer a seamless transition to debtcollection, and will even go so far as to prohibit TrueAccord from making any outbound calls or sending letters on their accounts because their customers have only ever interacted digitally.

This is because they must open a collection account on your credit report before they can begin pursuing you for payment. Collection accounts on your credit report can influence your credit score for up to seven years, even if you pay off the debt. This legislation is called the FairDebtCollection Practices Act.

If you have a debt that you haven’t paid yet, you may have heard from a debt collector called CCS Offices. CCS Offices is a company that collectsdebts on behalf of original creditor. They do this by either purchasing the debt or collecting the payments and taking a portion for themselves.

Collection accounts can hurt your credit score even after you pay off the debt. These entries remain on your credit report for up to seven years, which means that they can be viewed by creditors and lenders. Request Debt Validation. The debtcollection process is by no means perfect. Know Your Rights.

They are a third-party debt collector, which means that they may be hired by your original creditor, or they may purchase your old debt on the chance that you pay them instead. Here are the essential steps to take to stop their harassment and prevent them from damaging your credit score for years to come: Validate the Debt.

If you forget to pay a bill, the original creditor may move the debt to collections. This means that you may start to get phone calls from a debt collector like AAA Collections, harassing you to repay the debt. Getting rid of them can help you regain your credibility in the eyes of lenders.

Especially since the start of this year, many Americans have been struggling to manage their bills or make payments on existing debts. If you have had an overdue bill move to collections, you may begin hearing from a company called ACS Inc. A collections account on your credit report will cause your score to drop significantly.

Recently, the Consumer Financial Protection Bureau filed an Amicus Curiae brief in the United States Court of Appeals for the Third Circuit addressing whether a debt collector violates the FairDebtCollection Practices Act by accurately stating that it is seeking to collect $0.00 2:19-cv-18661 (2020)(Case No.

Debt collectors can cause a lot of problems for your credit score down the line. Collection accounts can hurt your credit score for up to seven years even after you pay off the debt. They can also be viewed by lenders down the line, which means you could be denied loans or credit cards.

When you owe money to a creditor or a service provider, it could result in a collections entry on your credit report. A collections entry can also result in tiresome phone calls and frequent letters until you make a payment. Asset Recovery Solutions, LLC, is a completely legit debtcollection agency headquartered in Illinois.

On April 21, the FairDebtCollection Practices for Servicemembers Act passed the House of Representatives under suspension of the rules. On April 14, Senators Sherrod Brown (D-OH) and Marco Rubio (R-FL) reintroduced the Small Business Lending Fairness Act. For more information, click here.

If you have heard from CACH LLC recently, they are likely pursuing you for an old debt. This means that they have either been hired by your old creditor or have acquired the debt from them to profit on your payments. Collection accounts are a black mark on your credit report. This can mean trouble for your credit score.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content