This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Proposed amendments to New York Citys rules governing debt collection have drawn significant scrutiny from trade groups outside the collection industry, most notably the American Financial Services Association (AFSA), which submitted a comment letter last week regarding the proposed amendments.

In part 1 of the series on trade-based money laundering (TBML) , we established a definition of the term, explored some recent studies and highlighted some typical techniques employed by the criminals. Efforts should also be made to raise financialinstitutions’ knowledge of TBML and related risks.

The Consumer Financial Protection Bureau has officially signaled it plans to rewrite its small business lending data collection rule, known as Section 1071, following major leadership changes earlier this year.

The Consumer Financial Protection Bureau (CFPB)’s decision to establish supervisory powers over nonbank financialinstitutions will level the playing field and subject those companies to much-needed scrutiny, credit union trade groups informed the agency Tuesday. Response From Credit Union Trade Groups.

The Federal Trade Commission on Friday announced it has amended the Safeguards Rule that will require non-bank financialinstitutions to report data breaches to the agency.

On October 27, the Federal Trade Commission (FTC) announced a final rule (Final Rule), amending the Standards for Safeguarding Customer Information (Safeguards Rule) under the Gramm-Leach-Bliley Act (GLBA) as it applies to covered financialinstitutions. Expanded Definition of “FinancialInstitution”.

A trade group representing non-bank financialinstitutions that provide sales-based financing to businesses has filed a lawsuit against the Consumer Financial Protection Bureau claiming it has overstepped its authority by issuing a rule regulating how lenders must collect and submit data related to small business lending activities.

Why it matters: As the student loan repayment landscape evolves, debt collectors and financialinstitutions need to understand borrower challenges to develop effective collection strategies and support financial wellness initiatives.

As per FTC, starting June 9, 2023 all collection agencies will be treated as financialinstitutions. When consumers turn to a financialinstitution for services, they want to know that their private information is being kept safe and sound. None of us want our information shared with companies we do not approve of.

Financialinstitutions are often required to make tough decisions when they receive the daunting Form 668–A, “Notice of Levy” from the IRS concerning a delinquent taxpayer’s bank account. FinancialInstitutions Tax Levy Obligations and Liability Exposure. By Austin Calhoun, Esq. and Joseph Luna, Esq. What is a Tax Levy?

Gramm-Leach-Bliley Act (GLBA) : This act requires financialinstitutions, including debt collection agencies, to explain their information-sharing practices to their customers and to safeguard sensitive data.

Sheri, a member of our Employee Benefits and Executive Compensation practice, provides our listeners with a 30,000-foot view of what equity incentive plans typically look like at a public company, such as a publicly traded bank or another financialinstitution.

In remarks this week at SEC Speaks, SEC Investor Advocate Rick Fleming mused that the “gamification” of securities trading might pose an undue risk that exploits a potential loophole in Regulation Best Interest (“Reg. He has over 35 years of experience representing financialinstitutions in litigation, regulatory, and compliance matters.

The current situation … poses serious compliance challenges for the membership of the Trades, as institutions that are identically subject to the [Final] Rule are now effectively subject to different compliance and implementation dates. Supreme Court term expected in July 2024.”

Where data has its own intrinsic value and where data breaches and cyberattacks are a risk for every business, the Safeguards Rule under the Gramm-Leach-Bliley Act (GLBA) provides financialinstitutions, including those in the accounts receivable management industry, with guidance on how to safeguard customer information.

CFS Partner Lori Sommerfield brings more than two decades of experience in representing a wide range of banks, financialinstitutions, and financial services companies in fair lending and responsible banking regulatory compliance.

As result of FTC lawsuit, federal court issues temporary restraining order halting scheme that sent fictitious debt collection notices to consumers nationwide As a result of a Federal Trade Commission lawsuit, a federal court hastemporarily haltedthe operations and frozen the assets of a phantom debt collection scheme and its operators.

The two special features of DeFi are: 1 It generated a robust global financial system on the crypto space geared by open-source technology. 2 It allows anyone to build financial applications without centralization of control. Similarly, users have more control over their data when compared to traditional financialinstitutions.

This filing comes just three days after CUNA and the National Association of Federally-Insured Credit Unions (NAFCU) sent a joint letter to the CFPB urging it to stay enforcement and implementation of the Final Rule for all covered financialinstitutions until after the U.S. CFPB (discussed here ).

Credit union and banking trade groups sent a joint letter to CFPB Director Rohit Chopra on Thursday to ask for additional data collection, development and analysis before making new overdraft policy recommendations. The post Trades Ask CFPB for More Data on Overdraft Protection Policy appeared first on Collection Industry News.

1960s: Credit reporting bureaus “sponsored” by banks or other financialinstitutions didn’t share information outside of their networks. Today, financialinstitutions have rules and policies to comply with different regulations and to protect their bottom lines. It’s not surprising.

The GLBA Data Protection Law The Gramm-Leach-Bliley Act, or GLBA, is a federal regulation to control how financialinstitutions collect, store, and transmit consumer information.

Investigators uncovered that Junaid Dar legitimately applied for a Bounce Bank Loan after he submitted accurate financial statements and in May 2020, received £13,000. However, Dar also applied for additional loans by applying to two separate financialinstitutions.

In 2015, the Federal Trade Commission came down on Chase for robo-signing affidavits. Chase was one of 13 financialinstitution censured for robo-signing documents in support of debt collection suits and foreclosure. Such is the case again with Chase. But robo-signing wasn’t just happening within Chase.

Security and Exchange Commission (SEC) treats cryptocurrencies as securities, Commodities and Futures Trading Regulator (CFTC) considers cryptocurrencies as commodities, and. have seized billions of dollars worth of cryptocurrencies to stop tax evasion, money laundering, false filling of tax returns, and trading illegal goods.

For instance, the insolvency practitioner may recommend a Company Voluntary Arrangement (CVA) if the business is able to keep trading while paying back its debts. What happens next depends on the company’s prospects. CVAs typically last up to five years but can bring a company out of debt.

On October 27, the Federal Trade Commission (FTC) announced a final rule amending the Standards for Safeguarding Customer Information (Safeguards Rule) under the Gramm-Leach-Bliley Act. The amendment will go into effect 180 days after publication of the final rule in the Federal Register.

On January 10, the Federal Trade Commission’s final rule , amending the Standards for Safeguarding Customer Information (Safeguards Rule) under the Gramm-Leach-Bliley Act (GLBA), became effective. Exempts financialinstitutions that collect customer information from fewer than 5,000 consumers from certain requirements.

Deceptive advertisements, market manipulation, misappropriation of customer funds, and “Ask Me Anything (AMA)” sessions served as the catalysts of a civil enforcement action the Federal Trade Commission (FTC) recently filed against bankrupt digital asset services provider Celsius Network LLC (Celsius) and its co-founders on July 13.

The CSA, the UK trade body for debt collection and debt purchase, has issued a detailed response to the Government in light of calls from a number of debt charities to call a halt to all collection activities and potentially write off billions of pounds of debt.

As we previously posted , on January 10, the Federal Trade Commission’s (FTC) final rule amending the Safeguards Rule under the Gramm-Leach-Bliley Act became effective. The updated Safeguards Rule will require more specific criteria for what safeguards financialinstitutions must implement as part of their information security programs.

But the American Bankers Association and Bank Policy Institute say the amendment as applied to financialinstitutions would duplicate existing regulations under the Dodd-Frank Act, while also requiring the turnover of a substantial amount of cybersecurity-related data that could prove dangerous in the wrong hands.

Supreme Court reverses the Fifth Circuit in Community Financial Services Association v CFPB (CFSA case), which found the CFPB’s funding structure unconstitutional. In a major victory for small business lenders, yesterday the U.S. CFPB injunction and those that were not covered, but the Bureau had not granted such petitions to date.

Chris, Lori, and Joe discuss who benefits from the injunction and what it means for those who do not, advocacy efforts by other financialinstitutiontrade groups to level the playing field, the impact on small business borrowers, when we can expect a resolution, and until then, how small business lenders should move forward.

By revising the Telemarketing Sales Rule (TSR), the Consumer Financial Protection Bureau (CFPB) and the Federal Trade Commission (FTC), along with state Attorneys General set forth a strict set of regulations that standardize the way all financial services companies in the debt relief industry must operate.

As the financial landscape continues to evolve, financialinstitutions and fintech businesses, including payment processors and money transmitters, are facing increased regulatory scrutiny and heightened consumer expectations.

Payment terms, interest rates, and rewards vary between financialinstitutions, but neither Visa nor Mastercard is inherently better. Both organizations are publicly traded —in May 2021, Visa had a $497.5 Issuers are financialinstitutions that actually issue cards. How Are Visa and Mastercard Similar?

Under the CFPB’s proposed timeline, SERs have only a few weeks to review the outline, which includes highly complex and sweeping changes to the FCRA that will fundamentally alter current practices and compliance regimes for businesses and financialinstitutions.” The trade groups requested a two-week extension to provide feedback.

Department of Education (ED) released an announcement about updates that postsecondary institutions must make to their cybersecurity and data protection policies in order to comply with the Federal Trade Commission’s amended Standards for Safeguarding Customer Information (Safeguards Rule), a component of the Gramm-Leach-Bliley Act (GLBA).

Chris and Kim explore the uptick in enforcement actions over the last year, the claims made in these cases, the SEC-imposed requirements and penalties on these companies, what we can expect going forward from the financial services regulators, and what financialinstitutions should do now to get ahead of these types of enforcement actions.

The People’s Bank of China (“PBOC”) announced this morning that it is banning crypto currencies and related services, including “trading, order matching, token issuance and derivatives for virtual currencies are strictly prohibited.” Tom is licensed in Tennessee, Texas, and Louisiana. See attorney profile.

If passed, the Responsible Financial Innovation Act would: Create definitions for crypto assets, payment stablecoins, smart contracts, distributed ledger technology, and similar important industry terms; Allocate enforcement authority for new crypto asset consumer protection requirements amongst the Commodity Futures Trading Commission (CFTC), Securities (..)

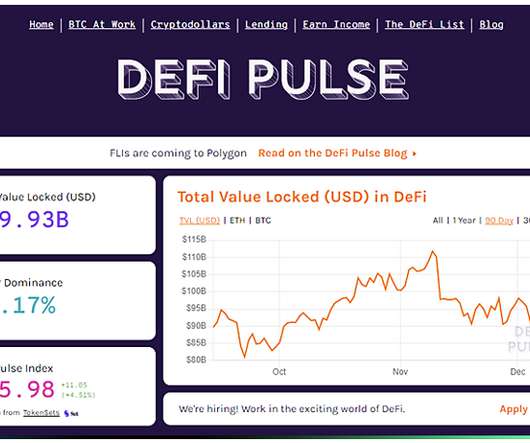

The report examines developments and associated vulnerabilities relating to three segments of crypto-asset markets: unbacked crypto-assets (such as Bitcoin); stablecoins; and decentralized finance (DeFi) and crypto-asset trading platforms.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content