This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

On May 1, the Federal Trade Commission (FTC) announced a permanent ban from debt relief telemarketing for operators of debt relief scam. The FTC charged the defendants with taking tens of millions of dollars from people by falsely promising to eliminate or substantially reduce their creditcarddebt.

According to the CFPB, on average, BNPL borrowers were much more likely to be highly indebted, revolve on their creditcards, have delinquencies in traditional credit products, have lower credit scores, and use high-interest financialservices such as payday, pawn, and overdraft compared to non-BNPL borrowers.

In 2021, the financialservices world continued to grapple with the uncertainty brought on by year two of the COVID-19 pandemic. In the first post of the series addressing whether minimum scoring criteria limits the consumers’ access to credit, Joanne Gaskin wrote: Simply put, the answer is no.

Increasing consumer debt levels are likely to propel the growth of the debt collection agencies market forward. Due to rising living expenses, easier access to credit, and post-pandemic reliance on loans, consumer debt levels are increasing.

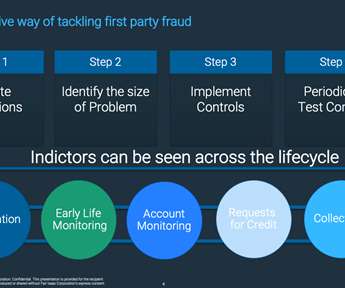

Or they may unintentionally sell it to criminal gangs, which then rack up thousands of pounds of fraudulent creditcarddebt. Furthermore, you might automatically assume that first-party fraud only affects banks, but as telcos evolve into payment processing and handset financiers, they also are now feeling the pinch.

The COVID-19 pandemic cast a huge shadow on the financialservices worldwide. We hope that what readers learned helped instill confidence in keeping credit flowing during uncertain times. consumers had on average $6,004 in creditcarddebt, down from an average of $6,934 back in January 2020.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content