This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Youve seen the headlines the federal government last week resumed collecting defaulted studentloan payments from millions of people for the first time since the start of the pandemic. How did we get to this point where so many people with studentloans are unable to make payments on them? for non-studentloan holders.

This net was driven by decreases in delinquent first mortgage and unsecured personalloan balances, which were offset by increases in delinquent bankcard balances and on a dollar basis in delinquent second mortgages. for this year, increased to 3.0% at the three-year horizon, and declined to 2.7% at the five-year horizon.

A personalloan is money borrowed from a lender that can be used for almost any purpose, from debt consolidation to home improvement projects. Most people don’t have $5,000+ sitting in their bank accounts—that’s where personalloans come in. What Is a PersonalLoan? Why Would I Need a PersonalLoan?

Economic stressors persist and are likely contributing to many consumers relying on credit to cover expenses, while the resumption of studentloan payments adds another financial obligation to the mix. banking system seems sound, inflation remains elevated. After three years of relief from payments on $1.6 a year ago.

Each year, tens of millions of Americans facing similar situations turn to personalloans to help ease the financial burden. With low interest for borrowers with strong credit scores, fixed rates, and a variety of lending sources to choose from, it’s easy to see why personalloans are so enticing. How PersonalLoans Work.

The best personalloans charge low fees and low fixed interest rates, have flexible loan amounts and terms, and have no prepayment penalties. A personalloan could let you access cash for any purpose. Since personalloans are unsecured, you’ll need an excellent credit score to get the best deal.

When your scholarships, grants, and federal studentloans aren’t enough to cover the cost of college, it may be time to turn to a private lender. Private studentloans can help you bear the weight of tuition. The key to finding the right studentloan with the lowest rates and best terms is to shop around.

The Prime Rate Good Mortgage Interest Rates Good Car Loan Interest Rates Good Credit Card Interest Rates Good PersonalLoan Interest Rates Good StudentLoan Interest Rates. This rate is largely determined by the federal funds rate, which is the rate banks charge each other. What Is the Prime Rate?

Credit builder loans aren’t great if you need the money now—since you need to pay off the loan before you can actually access the funds—but if you have time to build up your credit, they’re a great place to start. Passbook or CD Loans. Interest rates are typically much lower than credit cards or unsecured personalloans as well.

Bottom line: households took on more debt at the end of last year and we’re seeing loans increasingly going bad, according to data from the Federal Reserve Bank of New York , leading to a shift in consumer spending for 2024. million borrowers missed their studentloan payment, equating to 40% of loan holders.

25% despite concerns around the turmoil that has shaken the banking system , landing it at 4.75-5%. According to the Federal Reserve Bank of New York, U.S. The studentloan forgiveness debate continues into 2023 as the nearly 19% of Americans with studentloans wait to see how the case shakes out with the Supreme Court.

With tumult in the banking industry in Q2 and inflation and economic stressors persisting, the financial outlook for American consumers remains uncertain. The ending of various pandemic-era benefits including the pause on studentloan payments will impact consumers in the coming months. 9%) to $17.05 9%) to $17.05

You might take out a small personalloan to cover new band equipment, for example, or use a credit card to buy school supplies. Research studentloan options. It’s likely that you or your child will need to take out studentloans to pay for their education. on TD Bank's secure website. Card Details.

You can use credit cards to pay off different loan types, providing flexibility and potential benefits. Here are some common types of loans you can typically pay with a credit card: Personalloans: These unsecured loans can often be paid with a credit card, allowing you to consolidate debt or manage your monthly payments conveniently.

Auto Loans : Auto loans are issued by a bank, a credit union, or a company that specializes in automobile lending. Mortgage Loans: Mortgage loans are issued by a bank, a credit union, or a company that specializes in mortgage lending. Here are a few different types of installment accounts to consider.

on TD Bank's secure website. Mobile banking option Chime includes a plethora of tools designed to make your financial life much easier. The average debt load is broken into the following categories: $6,194 on credit cards $1,155 on store cards $16,259 on personalloans $19,231 on auto loan debt. Card Details.

Debit cards can help avoid overspending, as you cannot spend more than you have in your bank account. Monthly expenses might include studentloan payments, car payments, and credit card payments. Pay StudentLoan Debt. Even in bankruptcy, studentloan debt cannot get discharged; it must get paid.

While this can be a great way to build credit, it’s useful to know that this can also negatively affect your or the other person’s credit should either of you miss payments or over utilize the credit line. On your own, you may not receive approval on a personalloan or car loan.

According to Forbes, consumers owed $323 billion on personalloans in 2020. The banks limited loan opportunities because of the increasing risk of default. That’s why you’re charged lower interest rates on credit card balances you carry or loans you have. Starting and Owning a Business. Conclusion.

In recent years, the rise of digital lenders like SoFi and Ally has transformed the lending landscape, offering borrowers new options for obtaining loans quickly and conveniently. But what sets these digital lenders apart from traditional banks and credit unions? And how can you navigate the process of shopping for a loan with them?

For one, the consumer credit market is looking strong with signs of expansion, specifically, originations for credit cards and personalloans are increasing. As a result, originations for credit cards and personalloans have returned to pre-pandemic levels and have been holding fairly constant over the last two quarters.

BUSINESS WIRE)–An annual survey from Discover ® StudentLoans revealed that 58% of parents with college-bound students didn’t plan on applying for federal aid, but now have changed their minds. Parents bear a lot of the stress of paying for college, but so do students. Sheetal Shah, September 22, 2022. RIVERWOODS, Ill.–(BUSINESS

Credit cards, medical bills, and personalloans make up most unsecured debt that bankruptcy can eliminate. Studentloans, child support, recent taxes, and court fines must be paid in full. This type of bankruptcy often eliminates credit card debt, medical bills, and personalloans.

On Black Friday, Jason Apley was shopping with his wife when he checked his bank account and noticed he had about $500 less to spend than last holiday season. Unlike many Americans with crushing studentloan debt, the 44-year-old father of three from Knoxville, Tennessee, thought his debt had been canceled. This year, on Jan.

If the name FNB Omaha has appeared on your credit report recently, it’s likely because you submitted an application for a credit card with the First National Bank of Omaha. How to get a hard inquiry from the bank removed from your credit report. Home loans. Auto loans. Personalloans. Investment accounts.

StudentLoan Program Facing a $500 Billion Hole? trillion studentloan portfolio could be defaulted on. The article notes that the half trillion dollars of default would exceed what taxpayers lost on the saving-and-loan crisis 30 years ago. “Is the U.S. One Banker Thinks So.”. government’s $1.6

How Debt Consolidation Loans Work. A debt consolidation loan is a personalloan that can be used to pay off all of your debts, so instead of owing money to multiple sources, you will just have to pay back one lender with a monthly payment. When Might It Make Sense To Get A Debt Consolidation Loan.

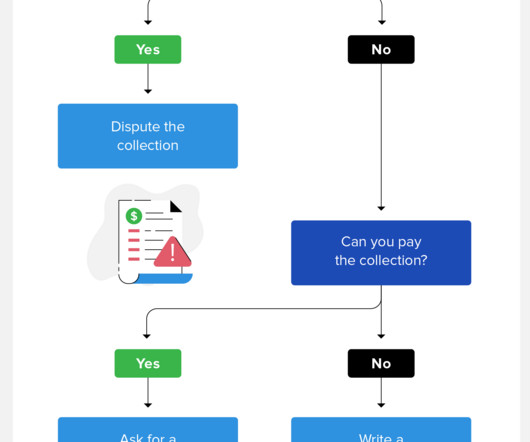

There are many kinds of debts that can be sent to collections, including: Credit card payments Studentloans Medical bills Rent payments Utility payments Auto loansPersonalloans Tax debt The time it takes the original creditor to transfer your debt to collections varies. This is done with a pay for delete letter.

Bottom line: households took on more debt at the end of last year and we’re seeing loans increasingly going bad, according to data from the Federal Reserve Bank of New York, leading to a shift in consumer spending for 2024. million borrowers missed their studentloan payment, equating to 40% of loan holders.

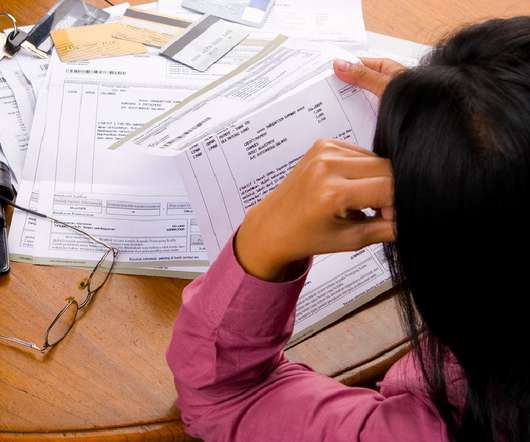

Next, you have to check your bank and financial statements to get an idea of your net worth. And, if you have both studentloans, and credit card debt, it may feel like a debt spiral. Look at your credit card statements and bank statements to know how much you have spent money and where. Types of Debt Consolidation Loans.

A debt management plan (DMP) is an agreement between a debtor (that’s you, the person in debt) and a creditor (think: your bank or your credit card company) that tackles your outstanding debt. Unsecured debts, such as credit cards, store cards and personalloans, can be part of your DMP.

Whether you’re carrying credit card debt, personalloans, or studentloans, one of the best ways to pay them down sooner is to make more than the minimum monthly payment. Doing so will not only help you save on interest throughout the life of your loan, but it will also speed up the payoff process.

It happens when the lender or bank associated with your credit card company checks your credit report to see if you are eligible for acceptance. Hard inquiries—or hard credit checks—occur whenever a lender or bank accesses your credit account. They’re also not usually visible to lenders or banks—only you.

Personalloan: Limited options. Auto loan: Limited options. The better news is that you could easily get an even more competitive loan with a little work to improve your credit. PersonalLoan Options with a 620 Credit Score. These financers often offer a lower APR than banks and other local lenders.

Studentloan. Personalloan. You’ve paid off a loan and, in so doing, changed your credit mix (loans to credit accounts). a mortgage or joint bank account) with someone who doesn’t have good credit. These include applications for a: Mortgage. Credit card. Apartment or house rental. Key Takeaways.

1.75% with the central bank expected to deliver more 50+ basis point rate hikes this year. Credit card balances are also already up year over year, reaching $841 billion in the first quarter of 2022, and are expected to keep rising, according to a report from the Federal Reserve Bank of New York. We all knew this was coming.

Certain debts—such as credit card debt, medical bills, and personalloans—can be discharged. The most common dischargeable debts include: Credit Card Debt: Unsecured credit card balances, including personal and store cards, can be discharged. It includes those taken for personal needs without collateral.

Loan approvals: Higher rates can make lenders more cautious, leading to increased loan denials, especially for those with lower credit scores. Savings and CDs: Savers can benefit from higher yields on savings accounts and CDs as banks seek deposits in response to Fed rate hikes.

Common types of unsecured debts include: Credit cards StudentloansPersonalloans Medical debt Back rent Utility bills Child support. These remedies can include garnishing your wages and bank accounts and seizing and selling your non-exempt personal property. Examples of Unsecured Debts.

It has taken actions to collect data on a number of new industries, including debt relief and earned wage access providers, and has filed a cease-and-desist order against a studentloan debt relief company charging borrowers exorbitant fees for the false promise of getting their student debt wiped.

If you qualify for Chapter 7 bankruptcy, our attorneys can guide you through the process of eliminating unsecured debts, such as credit card balances, medical expenses, and personalloans, within a matter of months. Studentloans are also difficult but not impossible to discharge in bankruptcy. How Much Debt Is Enough?

These levels refer to the total amount of money owed by individuals to creditors and encompass various forms of credit, including credit card debt, personalloans, mortgages, and auto loans which can significantly impact financial stability and economic conditions. increase compared to the fourth quarter of 2023.

If you allow the bank to take your house, these debts will be discharged. Most federal studentloans. Personalloans. Payday” type loans. Debts from willful and reckless acts, embezzlement, fraud, or larceny. HOA fees: As with your car and house debts, this depends on what you decide to do. Court fines.

Carrying debt, whether its through personalloans, credit cards, mortgages, or studentloans, is common in America. Here are some of the more common: Personalloans: These loans are typically issued by banks, credit unions, and online lenders. How Long Does Debt Consolidation Hurt Your Credit?

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content