This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Youve seen the headlines the federal government last week resumed collecting defaulted studentloan payments from millions of people for the first time since the start of the pandemic. How did we get to this point where so many people with studentloans are unable to make payments on them? for non-studentloan holders.

Economic stressors persist and are likely contributing to many consumers relying on credit to cover expenses, while the resumption of studentloan payments adds another financial obligation to the mix. trillion in student debt under the CARES Act, studentloan payments resume this month.

Your Chapter 13 bankruptcy plan creates an affordable route to satisfying your creditors and starting to rebuild your financial stability. The kinds of debt that can typically be eliminated are credit card debt, medical bills, utility bills, evictions, repossessions, and personalloans. It comes with some huge benefits.

The Prime Rate Good Mortgage Interest Rates Good Car Loan Interest Rates Good Credit Card Interest Rates Good PersonalLoan Interest Rates Good StudentLoan Interest Rates. What’s a Good Interest Rate on PersonalLoans? Personalloans are typically unsecured. In This Piece.

Can your family members’ creditors come after you now? Technically, personal debts aren’t forgiven at death. Instead, they pass to the estate of the deceased person. StudentLoan Debt. Federal studentloans and PLUS loans get discharged if borrowers pass away. Negotiate with Creditors.

With uncertainties about how the end of various pandemic-era benefits will impact consumers, it’s more important than ever for creditors and collectors to implement strategies that consider consumer situations and preferences when attempting to collect. If successful, many consumers will see their overall debt burden decrease.

The ending of various pandemic-era benefits including the pause on studentloan payments will impact consumers in the coming months. TrueAccord opinion, the court found that unlike telephone calls, two unwanted emails are insufficient to confer standing and wouldn’t be “highly offensive” to the reasonable person. 9%) to $17.05

If you file for Chapter 13 Bankruptcy in Indiana, you will still be obliged to pay something toward your debts; it’s just that you will be given a payment plan that reduces your unsecured debts based upon your ability to pay, that puts you on a manageable schedule, and that holds your creditors at bay while you work on making achievable payments.

You’ll also need to supply the bankruptcy court with a list of creditors, an income statement, and copies of your tax records. Filing Chapter 7 bankruptcy provides you with an automatic stay that prohibits creditors from being able to take any action to collect a debt against you, such as repossessions, wage garnishment, and legal action.

Bankruptcy will wipe out credit card debt, medical bills, and personalloans, but will not eliminate primary obligation debt; things like studentloans, child and spousal support, and newer tax debt. A Chapter 13 can help people get caught up on a mortgage or car loans. How Does Debt Negotiation Work?

Most creditors still report to old scoring models, so it’s unlikely paying off the debt will improve your credit score. If you’ve gotten behind on payments to a creditor or lender, your debt could be sent to collections after around 120 days of missed payments. ® or VantageScore 4.0®. This is done with a pay for delete letter.

There are exemptions depending on the property and how essential it is, but anything considered nonexempt will likely be sold to help pay off your creditors. Instead of discharging most of your debt and using your personal property to pay off creditors, a reorganization plan is filed to dela with the debt. StudentLoans.

Monthly expenses might include studentloan payments, car payments, and credit card payments. Pay StudentLoan Debt. Department of Education has extended loan payment forbearance, zero percent interest accrual, tax-free employer contribution benefits, and its pause on collections.

And, if you have both studentloans, and credit card debt, it may feel like a debt spiral. In this plan, credit counseling agencies negotiate with your creditors for arranging a customized and budget-friendly repayment plan for you. Based on your quote, they’ll negotiate with your creditors.

As part of the deal, they must mediate with the creditors to get their payments back on track. Personalloans. Pay day loans. A crisis or budgeting loan. Studentloans. Personal injury damages. Who is eligible? Store cards. Overdrafts. Debts from a confiscation order.

There are many different types of installment loans that are reported on credit reports. These include auto loans, mortgage loans, studentloans, credit builder loans, and personalloans. Creditors want to see whether you can handle different types of financing.

If you fail to pay, creditors cannot take your belongings. Credit cards, medical bills, and personalloans make up most unsecured debt that bankruptcy can eliminate. These debts have no collateral, so creditors cannot take your property without going to court first. This means there is no property tied to it.

Assets that do not fall within the statutory exemption values are liquidated and the proceeds used to pay your creditors something. A Special Note About StudentLoan Debt Can studentloans be discharged in bankruptcy?

These include transferring all your debt onto just one credit card as well as taking out a secured or unsecured personalloan—perhaps with the help of a professional debt consolidation company. Owing money to several creditors and remembering when the monthly payments are due for all of them can be overwhelming. Credit card 3.

If you miss payments and default on this type of debt, the creditor can seize the asset to liquidate it and apply those proceeds to the money you owe. In some cases, the assets or secured interest is something a creditor voluntarily agrees to in a lien; in other cases, the lien may be involuntary. Examples of Unsecured Debts.

When you file for Chapter 7 bankruptcy, the Court will place an automatic stay upon filing, which stops creditors from collecting payments, garnishing wages, or repossessing property. They will then determine what, if any, non-exempt property they can seize and will use the proceeds from that property to repay a percentage to your creditors.

How Debt Consolidation Loans Work. A debt consolidation loan is a personalloan that can be used to pay off all of your debts, so instead of owing money to multiple sources, you will just have to pay back one lender with a monthly payment. When Might It Make Sense To Get A Debt Consolidation Loan.

With a deep commitment to personalized service, we take the time to understand your unique circumstances and tailor our approach to your specific needs. This powerful solution can immediately halt creditor harassment, wage garnishments, and lawsuits, allowing you to breathe a sigh of relief and regain control of your financial life.

Creditors like to see that you can handle different types of debt responsibly. If you’ve only ever had revolving credit such as a credit card or store account, adding an installment loan can potentially bump your score up. In this situation, 43% of the person’s income is $1,505. Consider the example below.

A debt management plan (DMP) is an agreement between a debtor (that’s you, the person in debt) and a creditor (think: your bank or your credit card company) that tackles your outstanding debt. Unsecured debts, such as credit cards, store cards and personalloans, can be part of your DMP. Will creditors still contact me?

Debt is the amount of money you owe to a lender or creditor. Some examples of debt are mortgages, credit card dues, and personalloans. Although accruing lots of debt isn’t ideal, it may sometimes be unavoidable, such as mortgage payments or studentloans. What is Debt? You may be sent to collections.

This includes credit card balances, studentloans, medical bills, and other outstanding obligations. You gain a complete picture of your economic landscape by documenting each debt, including the creditor, outstanding balance, interest rate, and minimum monthly payment.

On your own, you may not receive approval on a personalloan or car loan. When you have a cosigner with a good credit score, the lender sees loaning to you as less of a risk because the cosigner is also attached to the loan. Should you find errors on your credit report, it’s your right to challenge them.

Creditors cannot reclaim any of your property if you default on a loan. a car or their home), and agrees that they will repay the loan in a timely fashion or else the lender will gain ownership of the collateral they used to get the loan. However, secured debt means the borrower has put up collateral (e.g.

Instead of fighting with your creditors, you work with them proactively in the bankruptcy process to resolve your debts. You have already paid your creditors at least as much as they would have received in a Chapter 7 bankruptcy , also known as a liquidation bankruptcy. Non-priority debts might include credit cards or a personalloan.

Creditors want to see that you can manage different types of accounts, such as revolving and installment accounts. Though employers will request permission for background checks, creditors can run a soft credit pull to prequalify you for marketing purposes. Research the creditor that authorized the hard inquiry.

Creditors give loans to millions of citizens, and thus credit companies are too busy to follow up on the debtors. For this reason, creditors are hiring debt collection agencies to collect debts that are 60 days past the agreed period. Therefore, the agencies act as middlemen collecting any delinquent loans.

This will immediately stop your creditors from being able to contact you to demand payment. You and your bankruptcy attorney will next attend either a creditor meeting or a 341 hearing with your court-appointed bankruptcy trustee. Most federal studentloans. Personalloans. Payday” type loans.

Studentloan. Personalloan. Lenders and creditors report new information about your activity to the credit bureaus. It also helps to know which everyday financial activities require hard checks, so you can go through with them only when you’re really serious. These include applications for a: Mortgage.

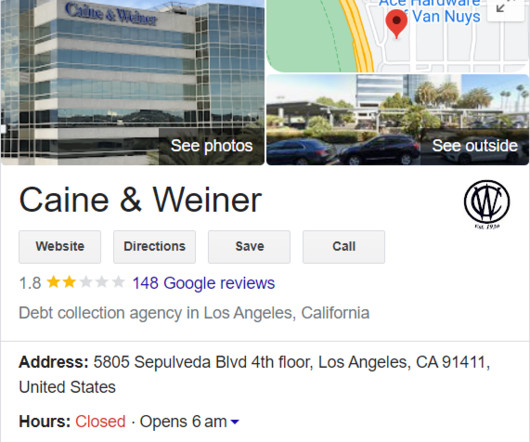

Caine and Weiner is a prominent debt collection firm that operates across various sectors, gathering debts from a range of industries, including: Personalloans Phone bills Studentloans Credit cards To secure his debts, Caine and Weiner acquire them from the original creditors at a reduced price, then pursue the entire amount from the debtor.

We examined a large, nationally representative sample of millions of consumers from October 2020 to test the ability of FICO® Resilience Index (calculated before the COVID-19 crisis started, as of January 2020) to rank order the likelihood of currently-in-force creditor accommodations.

These levels refer to the total amount of money owed by individuals to creditors and encompass various forms of credit, including credit card debt, personalloans, mortgages, and auto loans which can significantly impact financial stability and economic conditions. increase compared to the fourth quarter of 2023.

Certain debts—such as credit card debt, medical bills, and personalloans—can be discharged. Chapter 7 Bankruptcy The liquidation process is managed by a trustee who sells non-exempt assets to pay creditors. Many personal assets may be exempt. It includes those taken for personal needs without collateral.

The court will then order a bankruptcy stay — also called an automatic stay — that prohibits creditors and lenders from collecting what you owe. This plan states that you’re committed to paying back something to creditors in monthly installments, and you detail the minimum amount you’ll pay as well as the duration of the plan.

Once the trustee receives these funds, they then pass them on to creditors to put toward your debt. If a prospective debtor is not eligible for a Chapter 7, a Chapter 13 can force creditors to take what the law requires they pay them, and then they can get a discharge at the end of the plan on the unpaid balance of most unsecured debts.

The types of credit accounts you can expect to see in this section include: Mortgages , home equity loans, and home equity lines of credit. StudentLoans. Auto Loans. PersonalLoans or Other Installment Loans. Your creditors will report on your credit accounts regularly. Credit Cards.

When writing your budget and listing all your outstanding debts, work out which of those debts are incurring further fees and interest, such as credit cards and loans. Don’t be afraid of approaching your creditors and debt collectors and talking to them. Put them at the top of your list. Everything else can wait. .

The money earned from these sales then goes to the creditors and any remaining balances on the debts are discharged. If the court grants a judgment in favor of the creditor, they have additional collection options, such as wage garnishment, bank account levies, or placing liens on the debtor’s property. What Are My Exempt Assets?

If you don’t have a card with a high enough limit to keep you comfortably under 25% utilization, give the creditor a call and request that they up the credit limit. You Need a Mortgage Loan. You definitely don’t need a mortgage loan to have good credit. Don’t Apply for Loans or Credit Cards for at Least a Year.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content