This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

When account owners have an account that reflects a negative balance, the lender is faced with a myriad of options and obligations with regard to the pursuit of that debt. Lenders that charge off a debt trigger issuance of the 1099-C when their defined policy leads the lender to discontinue collection activity and discharge a debt.

Many people assume that because they have filed bankruptcy, their credit is ruined, and they will not be able to qualify for any loans. There are a number of steps you can take to improve your credit score and to make it likely that you can be approved for a loan. 15% Length of credit history. 10% Credit mix.

Bankruptcy can happen to anyone—despite their best efforts. And while most people understand that bankruptcy is generally bad for them, many don’t realize the details of how it can impact you. Read below to find out what happens to your credit score after bankruptcy and what you can do to repair your credit afterward.

When filing for bankruptcy, you can discharge certain types of personal loans, meaning that you’re no longer legally responsible for paying off the debt. If you’re considering filing for bankruptcy, you need to know what personal loans you can discharge and which filing method suits your financial situation.

The CFPB has the authority to stretch its long arm as far as the most remote corner of the United States and its territories in order to supervise and audit local banks, creditunions, payday lenders, debt collection agencies, and more.

n]: A financially detrimental debt arrangement that only benefits the lender. Unfortunately, while the former is pretty straightforward, there’s a lot of confusion surrounding the latter – something that shady or disreputable lenders use to their advantage. And storefront operations can run differently than online lenders.

Trying to get approved for credit can be a sort of Catch-22: Creditors want proof that you’ve handled a credit card well before, but without a credit card already in hand it can be hard to show you’re a good risk. What Is A Credit Builder Loan. How Credit Builder Loans Work. Who Needs a Credit Builder Loan?

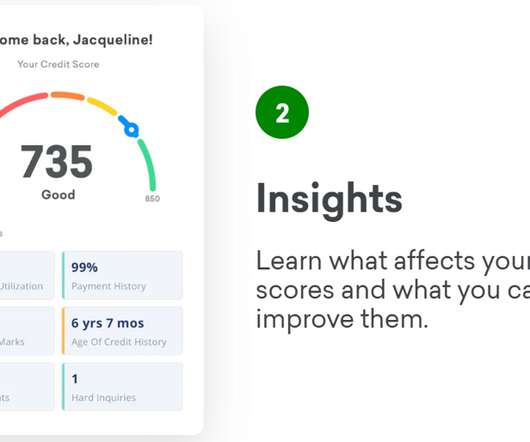

At any given point, we may have several credit scores based on our financial history, as measured by companies such as FICO or VantageScore Solutions, another credit analysis company. Experian reports that the lowest FICO credit score is 300, but no one really stays at such a low score once some financial history has been established.

In July 2016, the Consumer Federation of America (CFA) and VantageScore Solutions reported that most consumers—more than 80%—knew basic facts about their credit scores, including that credit scores are used by lenders to approve or deny mortgages and by credit card issuers to approve or deny credit cards.

This code can mean two different things: You don’t have enough accounts for lenders or credit scoring models to effectively gauge your risk as a borrower. Even if you’ve paid your bills on time, if you only have one credit card that’s been open three months, that’s not enough information for many lenders.

Chapter 13 bankruptcy is an invaluable financial tool for those struggling with overwhelming debt, and it can pave the way for a fresh start. Unlike Chapter 7 , Chapter 13 bankruptcy allows you to avoid liquidating your non-exempt assets. What Is a Chapter 13 Bankruptcy Filing?

A good credit score is essential if you’re looking to get approved for anything from a rewards credit card to a mortgage. But what score do lenders consider to be good? If you have a 560 credit score, your approval odds for loans are low, and your credit rating is pretty poor. Bankruptcy. Repossessions.

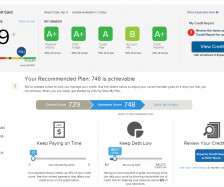

Improve score : You’ll need a good credit score (of around 670 or higher) to get a loan or credit card with a low enough interest rate. If your score is low, you’ll need to know how to fix a bad credit score before going through the application process. Bankruptcy. Debt settlement.

Individuals with “fair” credit scores usually have late payments on their credit reports , some of which may have gone to collections. Others are on the path to repairing their credit, as it takes time to recover from more severe credit occurrences like bankruptcy , foreclosures , or judgments. downpayment.

A 1099-c cancellation of debt form is issued when a lender forgives or cancels a debt. So, while getting a 1099-C itself doesn’t change your credit at all, you’ve probably already experienced a negative hit to your score. You must also be an applicable financial entity, such as a bank or creditunion.

Having a bad credit score can make it difficult to get a loan. “A bad credit score is somewhat of an indicator of your short, medium, and long-term ability to repay the loan, which is how banks make money.” LendingTree is an online marketplace that connects borrowers with different lenders across the country.

Having a bad credit score can make it difficult to get a loan. “A bad credit score is somewhat of an indicator of your short, medium, and long-term ability to repay the loan, which is how banks make money.” LendingTree is an online marketplace that connects borrowers with different lenders across the country.

Debt consolidation is the process of taking out a loan or a new line of credit and using the funds to pay off or dramatically reduce your current debts, ideally at a lower interest rate or with a lower monthly payment. This could help you pay off what you owe faster, get out of debt, and improve your total credit utilization ratio.

In addition to keeping your credit utilization low, to begin with, you can improve your credit score by paying down large credit card balances, which shows lenders that you aren’t a risky borrower. Length of Credit History: 15% of Credit Score. New Inquiries: 10% of Credit Score.

The Consumer Financial Protection Bureau (CFPB) has had its hands full overseeing actors across sectors–from regional and large banks to auto and online lenders to mortgage and credit agencies–in an ongoing effort to protect consumers in an ever-growing landscape of financial product offerings. And currently, approximately 4.7%

Pay it off with a debt consolidation loan A debt consolidation loan from a bank, creditunion or online lender may also be worth considering. This type of borrowing allows you to take out a new fixed-rate loan to pay off multiple credit cards, consolidating revolving debt into one installment payment.

Common reasons for bank account garnishment in Texas include: Private creditors: These are banks, creditunions, credit card companies, peer-to-peer lenders, hard money loan providers, and other financial institutions. This debt can include anything from credit cards to past due balances on office space.

On January 12, the Financial Crimes Enforcement Network (FinCEN) republished frequently asked questions (FAQs) regarding the implementation of the Paycheck Protection Program (PPP), the requirements of the Bank Secrecy Act, and how lenders may adhere to those requirements when issuing a PPP loan. For more information, click here.

On January 11, the Consumer Financial Protection Bureau (CFPB) proposed a rule to establish a public registry of supervised nonbanks’ terms and conditions in “take it or leave it” form contracts that claim to waive or limit consumer rights and protections, such as bankruptcy rights, liability amounts, or complaint rights.

On January 19, the Federal Court of Appeals for the Third Circuit ordered the bankruptcy court adjudicating the bankruptcy of FTX to appoint an examiner to investigate the collapse of the digital asset exchange. For more information, click here. For more information, click here. For more information, click here.

The reason: Interest rates are how credit card companies manage the risk that a customer won’t pay their credit card bill on time. Generally, customers with lower credit scores are deemed riskier to lend to. To compensate, lenders tend to charge higher rates compared to borrowers who have a score in the upper range.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content