This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

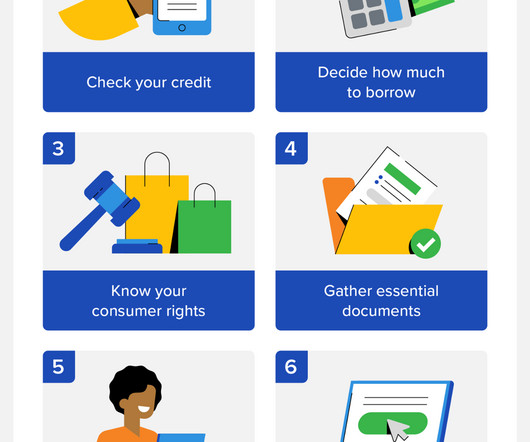

Debtconsolidation combines multiple debts into a single, more manageable payment, often with a lower interest rate. This can be done through loans, balance transfers, or other methods. Are you tired of juggling multiple monthly payments on high-interest debts? If so, debtconsolidation might be the answer.

Debtconsolidation is when you bundle several debts together into one larger sum and then make a single monthly repayment instead of multiple smaller ones. Consolidatingdebts with different interest rates and repayment schedules can make it easier to manage your finances. DebtConsolidation Guide.

When you are overwhelmed by debt, you may start to wonder if declaring bankruptcy or pursuing debtconsolidation is the better option. Understanding the key aspects of each can help you determine what is better, bankruptcy or debtconsolidation, for your situation. Equity loans put your home at risk as collateral.

A personal loan is money borrowed from a lender that can be used for almost any purpose, from debtconsolidation to home improvement projects. Most people don’t have $5,000+ sitting in their bank accounts—that’s where personal loans come in. You may even qualify for a subsidized loan or an income-driven repayment plan.

Loan Terms. Life Insurance, StudentLoan Refi, Credit Card Comparisons. How Does A Fiona Loan Work? Fiona works as an aggregator for personal loan lenders ; it does not actually fund any personal loans itself. StudentLoan Refinancing. Desired loan amount. 24 – 84 months. Cost to Use.

You aren’t allowed to pick and choose which debt you want the bankruptcy to apply to. Briefly, unsecured debts are not backed by any collateral and include things like credit card balances and unpaid medical bills. Creditors cannot reclaim any of your property if you default on a loan. What is my total credit card debt?

Everything about personal loans is fixed from day one: the length of the loan, the interest rate, and the amount you borrow, meaning the terms of your loan are set in stone. Personal loans can be either secured or unsecured. The far more appealing choice, the unsecured personal loan, does not require any collateral.

The best personal loans charge low fees and low fixed interest rates, have flexible loan amounts and terms, and have no prepayment penalties. A personal loan could let you access cash for any purpose. Since personal loans are unsecured, you’ll need an excellent credit score to get the best deal. Compare Rates Now.

Bankruptcy filers with income below their state’s median can potentially qualify for Chapter 7 to discharge many debts. However, certain debts like child support, alimony, and other domestic support obligations cannot be eliminated. Studentloans are also difficult but not impossible to discharge in bankruptcy.

Household Debt Is at an All-Time High Household debt across all categories grew by 4.8% This includes mortgages, home equity revolving debt, auto loans, credit cards, studentloans and other consumer lending such as retail cards. The total household debt of $17.3 over the same period. on the year. “It

The largest increase in any category was credit card debt, which swelled by 16.6% Auto loan and mortgage debt increased by 4%, while studentloandebt saw a modest rise of 1.6%. It is important to remember that household debt is primarily composed of mortgages, auto loans, credit cards and studentloans.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content