This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

When filing Chapter7 or Chapter 13 bankruptcy, it’s critical to understand the difference between consumer debt and non-consumer debt. If you’re considering filing Chapter7 or Chapter 13 bankruptcy, consider enlisting the help of skilled bankruptcy attorneys.

If you fail to repay an unsecured personal loan, the lender cannot repossess your assets. Common unsecured loans include: Bank loans with no collateral. Repossession deficiency claims. Discharging Personal Loans Through Chapter7Bankruptcy. Unsecured loans are loans that don’t have collateral. Payday loans.

Chapter7bankruptcy is a great financial solution for those struggling with debt, especially unsecured debts. With Chapter7bankruptcy, you as the debtor can discharge most unsecured obligations after liquidating nonexempt assets. What Is Chapter7Bankruptcy?

They will feel obligated to protect their interest in the collateral (your car) and can move quickly to repossess after only a few missed payments. To speak with a Colorado attorney experienced in debt relief and bankruptcy, call The Law Office of Clark Daniel Dray at (303) 900-8598 or use the tool below to scheduled a free consultation.

Those filing an emergency bankruptcy receive an automatic stay even before completing certain documents. If you’re in an emergency situation such as wage garnishment, eviction, or pending repossession filing an emergency bankruptcy may be right for you.

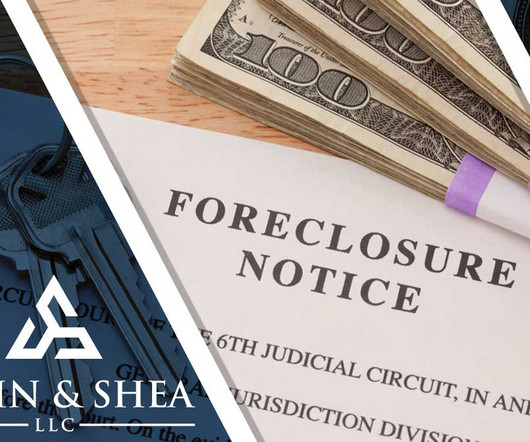

Whether you’re facing foreclosure , repossession, wage garnishments, or relentless creditor harassment, our expertise in bankruptcy law can offer the protection and relief you’ve been seeking. One of our firm’s key strengths lies in our comprehensive understanding of both Chapter7 and Chapter 13 bankruptcy options.

If you choose bankruptcy, there are also different options depending on whether you choose a Chapter 13 bankruptcy or a Chapter7bankruptcy. If you are facing foreclosure or bankruptcy, the best way to determine which choice is right for you is to speak with an experienced bankruptcy attorney.

Although businesses can also declare bankruptcy, we will focus on personal bankruptcy in this article. In Chapter7Bankruptcy , (sometimes misleadingly described as liquidation bankruptcy), certain debts are discharged within 3-4 months. Chapter 13 Bankruptcy is sometimes called “the wage earner’s plan.”

In this blog, we’ll discuss how Chapter 13 usually affects credit scores, and we’ll give you actionable tips to begin rebuilding your credit. If you have additional questions regarding Chapter 13 or Chapter7bankruptcy, contact the attorneys at Sawin & Shea, LLC.

financial assets (including bank accounts and investments), debts owed to you (including tax refunds, loans, and other obligations), assets related to your business, and any other assets you may own. In Colorado, they choose which assets you are permitted to keep in your bankruptcy case. You can start over because of that.

Banks can seize business assets and liquidate as a last resort to cut their losses. Missing payments on secured debt causes the creditor to repossess the property as recourse. Retailers Gymboree, Charlotte Russe, Payless, Roberto Cavalli, and Diesel filed Chapter7bankruptcies in 2019. The question is who?

To enforce secured debts, your creditors may repossess your car or other vehicles, they may foreclose on your mortgage, or levy against other property you have either pledged as collateral or that is subject to an involuntary lien. What collection remedies are allowed will vary by state.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content