Consumer advisory: Don’t give money or information to scammers promising student loan forgiveness

Recognizing student loan scams

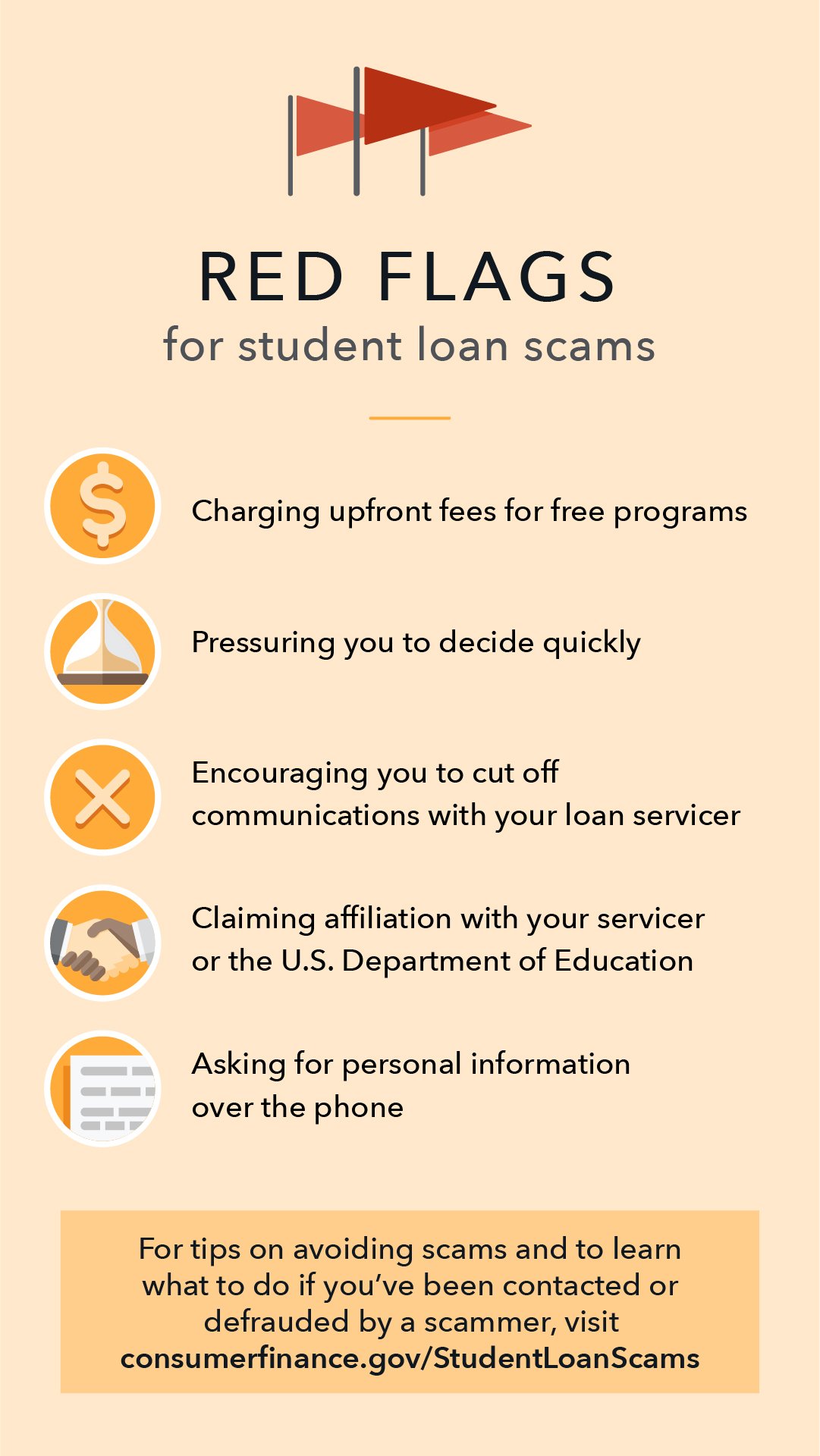

Our infographic highlights red flags for student loan borrowers to watch out for.

{kind=link}

Numerous student loan borrowers recently submitted complaints to the Consumer Financial Protection Bureau (CFPB) about companies that promised them student loan forgiveness or loan forbearance in exchange for fees amounting to hundreds or thousands of dollars. Borrowers believed they were talking to their servicer or a company authorized by the Department of Education because they often knew private information such as the borrower’s loan balance or recent consolidation activity. This is fraud.

Legitimate options for getting rid of your federal student loans as of August 2022:

- Loan forgiveness is not available for all student loan borrowers at this time, though there are programs to forgive federal student loans for specific borrowers , such as public service employees, and discharge loans in other circumstances . On August 24, 2022, it was announced that borrowers with federally held loans and incomes under $125,000 (individuals) or $250,000 (married couples or heads of household) can apply for up to $10,000 in student debt cancellation—or up to $20,000 if they received a Pell Grant in college. Learn more about the Biden-Harris Administration's Student Debt Relief Plan .

- Federal student loan servicers cannot charge you to apply for loan forgiveness, income-driven repayment (IDR), deferment, or forbearance, or to file any other paperwork. Federal loan servicers do not charge any application or processing fees to consolidate your federal loans into a Direct Consolidation Loan.

- The CARES Act pause on payments and interest for federally held student loans has been extended through December 31, 2022. Forbearance on qualifying loans will happen automatically. No one will contact you to sign up for CARES Act forbearance. There is no fee to enroll in CARES Act forbearance. If your payment will be too high when the pause ends, please reach out to your servicer directly to explore a variety of payment relief options. Your federal loan servicer will not charge you any application or processing fees to help you switch to a different repayment plan such as an IDR plan or enroll in any of the deferment or forbearance options available to you.

In addition to submitting complaints to the CFPB and the Federal Trade Commission (FTC) , we encourage consumers to learn how to recognize these scams and how to report scammers to authorities.

Here are some red flags to watch out for

Charging upfront fees for free programs

Scammers often attempt to charge for programs that all borrowers can access for free, including preparing the paperwork. Loan forgiveness or discharge (to the extent those programs are available to you), loan consolidation , student loan forbearance and deferment are all free programs provided by your servicer. If a company is asking you to pay large amounts of money upfront, it is likely a scam and should be reported. Do not give any money or personal information to the company. Contact your loan servicer to determine what options are available to you. You can find out who your servicer is by logging in to your Federal Student Aid account or calling 1-800-433-3243.

Pressure to decide quickly

Scammers might tell you that you only have 24 hours to take advantage of an offer or program. This is a red flag. Most government-offered programs do not require this sense of urgency. Confirm whether this is a legitimate company before you take any additional steps.

Encouraging you to cut off communications with your loan servicer

This is warning sign that this company is not working in your best interest. As a student loan borrower, it's important for you to maintain communication with your servicer. If someone urges you to make payments to their company instead of your loan servicer or to stop communicating with your loan servicer, do not give them any information. Do not stop making payments to your servicer.

Claiming to be affiliated with your loan servicer or Department of Education

Scammers might name drop organizations that you have a loan account with. Be careful of statements like “we work with Department of Education” or “we’re partnered with your loan servicer.” If someone contacts you and claims to be partnered with your loan servicer, hang up the phone and contact your loan servicer directly to confirm. Call the number provided on your billing statement or through your servicer’s web portal. Do not use contact information provided in an email or voicemail message.

There might be times when your student loan servicer contacts you about Public Service Loan Forgiveness (PSLF). As part of a recent settlement with the CFPB, Edfinancial, a federal student loan servicer, is required to contact all of its Federal Family Education Loan Program (FFELP) borrowers to inform them of the limited PSLF waiver so that eligible borrowers can take advantage of the waiver before it expires.

Asking for personal information via email or over the phone

Scammers often ask for personal information like your full Social Security number, bank account number, FSA ID or studentaid.gov password. Do not give any personal information to an unverified company over the phone. If you suspect the caller may be a scammer, hang up and contact your servicer directly to determine if there are any actions required for your loan. If you have provided your personal information to a scammer, we have listed some tips for avoiding scams below.

Tips for avoiding scams

- The person contacting you might have correct information about you or your loan, but that doesn’t mean they’re legitimate. Some scammers knew the borrower’s loan balance or about their recent application for consolidation. This led borrowers to believe they were talking to their servicer or another legitimate entity.

- Don’t share your personal information. Consumers reported being asked for their Social Security number, bank information, FSA ID, and studentaid.gov login information. This allows them to steal your money and cut you off from your servicer, so they can’t notify you of missed payments.

- Don’t sign a power of attorney. Some consumers have been asked to sign a power of attorney allowing the company to deal with the student loan servicer on their behalf. This allows them to make financial decisions for you. Don’t give this power to someone unless you know them personally and trust them!

- Stay in contact with your servicer. Sign into your student loan servicer’s web portal to periodically check in on your loans. Any notices for your student loans will be available through your servicer’s website.

- Take your time. An honest company will not pressure you to make a decision quickly. If you’re unsure, end the conversation and research the company to confirm whether or not they are legitimate.

- Keep track of your student loans. Student loans can be confusing, and scammers rely on that. If you know the types of loans you have and who your servicer is, it’s harder for scammers to take advantage.

If you’ve been contacted by a scammer or defrauded

- Cancel your payments. If you realize after the fact, work with your bank to cancel or block your scheduled payment. Your bank should have policies in place to help you avoid future fraudulent activity.

- Contact your servicer. They can help you protect your account. If you signed a power of attorney giving the scammer the right to communicate with your servicer on your behalf, get it revoked.

- Submit a report to the Federal Trade Commission (FTC) . In addition to reporting your complaint with FTC you can contact Department of Education Office of Inspector General.

- Contact state officials. Let the Attorney General in your state know. Contact your state student loan ombudsman if you have one.

For additional information regarding student loan scams and actions the Bureau and the FTC have taken against scammers, please see the 2019 Education Loan Ombudsman Annual Report .