Black History Month is a time for reflection, celebration, and truth telling of the progress of Black people and the continued economic inequities that persist. The Black Wealth Data Center was launched to empower community practitioners and decision-makers to leverage reliable data in understanding and addressing the economic and wealth barriers the Black community is experiencing.

We have recently witnessed historical events for the Black community, specifically by Black women. From Kamala Harris being the first women of color elected Vice President of the United States to Judge Ketanji Brown Jackson becoming the first Black women to serve in the U.S. Supreme Court. While both reflect the power and strides of Black women in America, they are a minority. Black women are still highly underrepresented in leadership at all levels and continue to face economic and wealth building barriers.

Ebony: What does the data say about the state of Black women? Let’s start with what’s going well.

Natalie: Black women are earning education credentials and getting jobs in fast-growing fields. Between 2011 and 2019, the percentage increase in bachelor’s degree attainment for Black women outpaced that of White women and Asian women.

Black women aged 25-34 who earn a bachelor’s degree in a STEM field end up working in a STEM field at about the same rate (25.0%) as White (26.2%) and Hispanic (24.9%) women.

What are you seeing when you look at the data?

Ebony: According to the 2019 State of Women-Owned Business Report from American Express, Black women are the fastest-growing group of entrepreneurs. While the number of women-owned businesses grew 21% from 2014 to 2019, Black women-owned businesses more than doubled during that time at 50%.

However, starting and running a business comes with many institutional barriers and biases and it’s evident that the full potential of economic growth for Black women and the communities they reside in has not been fully realized.

What concerns you when looking at the data?

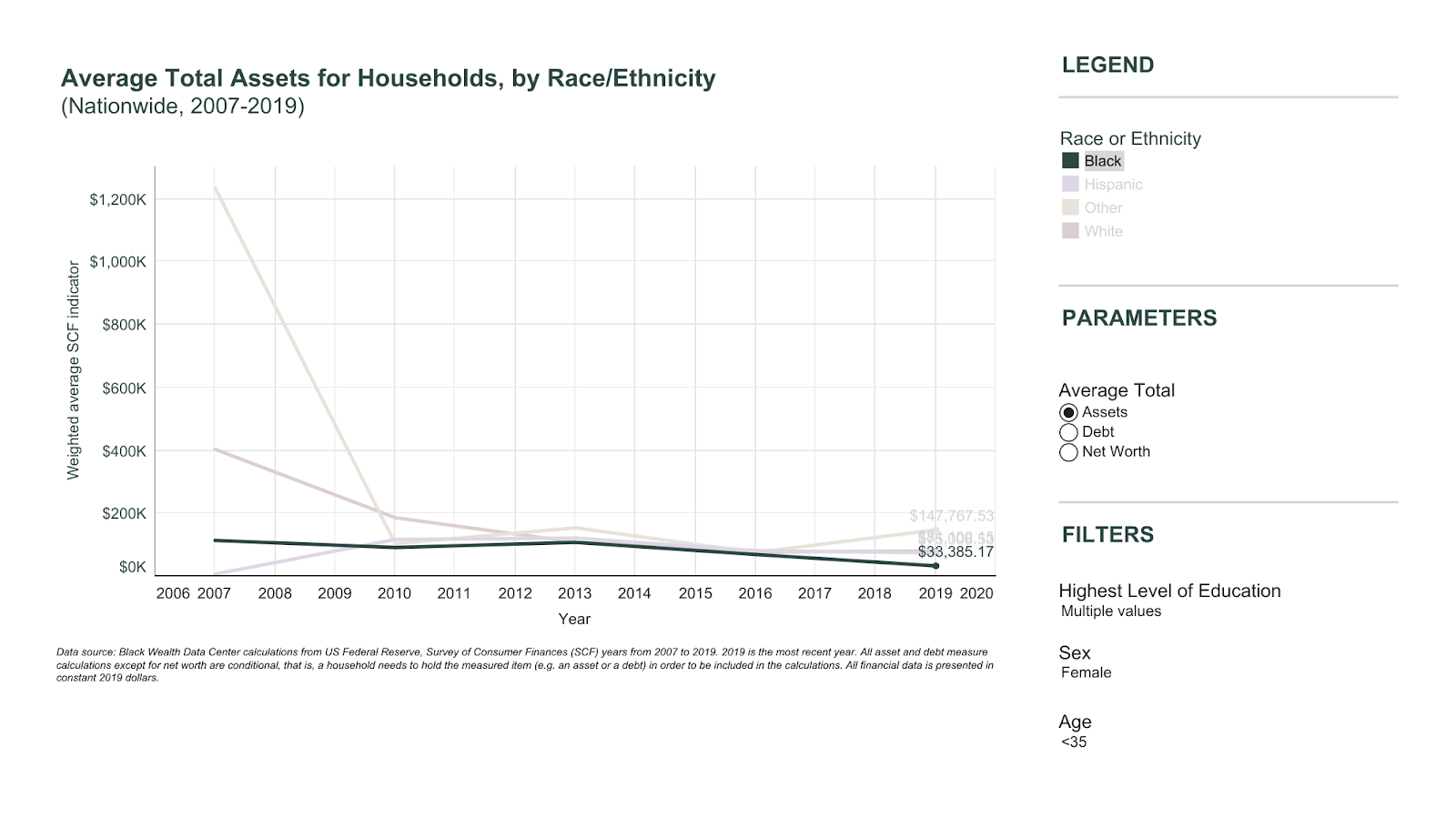

Natalie: Judging by a handful of primary economic indicators, Black women are struggling financially. Our Racial Wealth Equity Database looks at Black women’s total assets from 2007 – before the recession – through 2019 – before the pandemic.

Over that period of time, the average total assets for Black women decreased by 37%, the largest of any decrease among women of all races.

Younger Black women fared worse than older Black women. Between 2007-2019, the average total assets for Black women under the age of 35 of all educational levels decreased by more than 50%, from $58,000 to $22,000. For comparison, during that same time period, Hispanic women under the age of 35 of all educational levels increased their total assets from $19,000 to $63,000 (exceeding white women of similar age and educational attainment).

Alarmingly, this trend holds even for Black women who earned post-secondary degrees. In 2007, the average total assets for households led by college-educated Black women under the age of 35 was $114,000. In 2019, the average total assets had fallen to $33,000.

What will you be keeping an eye on during 2023, particularly with fears of a recession?

Ebony: We have spoken about the success of Black women in surpassing other groups in earning education credentials and exploring entrepreneurship - both coupled with some hard financial realities that lead to increased debt and hardship.

For example, Black women borrowers are the group most negatively affected by student loans. Those who completed a four-year degree graduated with an average of about $38,000 in student debt, compared to around $35,000 for Black men and $27,000 and $24,000 for white women and men respectively. This disparity only widens when looking at debt after graduate education.

In the same vein, many Black women entrepreneurs invest their own money due to lack of access to financial support, networks and markets. Because Black women exist at the intersection of two marginalized identities and experience sexism and racism at the same time, they usually make less money as a group and experience bias that derail economic and wealth building mobility. While earning slightly more than Hispanic women ($39,511), Black women in 2021 earned on average $46, 543 annually, which is lower than White women ($51,451) and Asian American women ($63,867). In comparison, the median annual earning for men overall was $61,180, according to the U.S. Department of Labor.

Natalie: Well, I’ll be keeping an eye out as new data is released, and I know you will be, too. Readers can subscribe to the Black Wealth Data Center’s newsletter to learn when we release site updates, and they can also reach out to us at [email protected] to inquire about office hours, explore partnership opportunities, and much, much more.

Ebony: Yes, not only will I be looking at new data trends, I will be paying close attention to programmatic strategies, policies, and investment priorities of key actors and partners who are having success in decreasing financial burdens on Black women. For those interested in learning more about the interconnections of household financial health, racial economic equity and policy, I would check out Prosperity Now’s Scorecard and join our community to get the latest reports and tools.

Related Content

This Fair Housing Month, We Demand Housing Justice

This April marks the 56th anniversary of the Fair Housing Act, a landmark piece of legislation which outlawed housing discrimination...

Apr 2024

A Bright Future for Baby Bonds

In January 2022, Prosperity Now and the Institute on Race, Power and Political Economy at the New School collaborated on...

Feb 2024

Financial Empowerment for the Underserved: An Interview with Adrian Gomez of United Way of Pueblo County, Bank On Pueblo County

Bank On Pueblo County, a component of United Way of Pueblo County located in Pueblo, Colorado, is a coalition working...

Feb 2024

Tracing the Evolution of Racial Wealth Inequality and Economic Mobility in America

Historical injustices and systemic barriers have continued to hinder the economic progress of Black Americans, reflected in the enduring racial...

Feb 2024