All companies take payments but many don’t understand how the payment industry works behind-the-scenes. The digital payments landscape is complex, and with new technologies emerging, the greater payment ecosystem continues to evolve.

It’s true you don’t need to be a payment expert to run a business, manage an office or head up an accounts receivable team. However, being familiar with the journey your payments take can:

- Help you understand your payment fees and billing models

- Help you predict when funds will be available in your merchant account

- Help you fight chargebacks and prevent them in the future

- Help you make educated decisions about which payment communication software to use

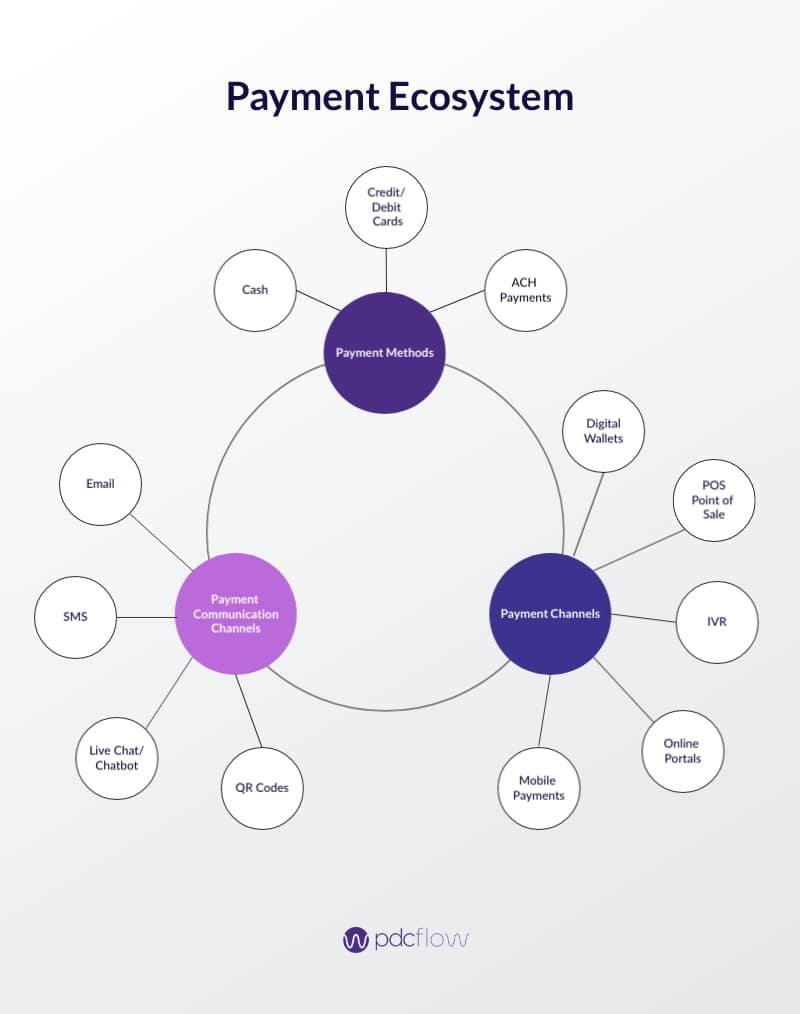

What Makes Up the Payment Ecosystem?

For companies, the most important element of the payment ecosystem is how your business gets paid: credit card, ACH, cash, or less commonly, paypal or digital wallets.

The other component organizations should understand is the ideal method for collecting payments: email, SMS, chat, online payment portal, QR codes on letters, staff-assisted transactions, etc.

PAYMENT METHODS

Cash

Taking cash is usually straightforward. Even businesses without a typical storefront location or traditional point of sale register can accept money using cash tracking features within their payment software.

Credit Cards

Merchants can be wary of accepting credit cards because of the fees associated. The reality is, though, if you’re not making it easy for customers to pay you will drive them to competitors who provide a customer centric experience people have learned to expect.

ACH Payments

Making an electronic payment from a bank account is the other major payment option you can provide to customers. Offering both credit card and ACH is standard for most businesses. The more options you give your customers, the more transactions you’ll bring in.

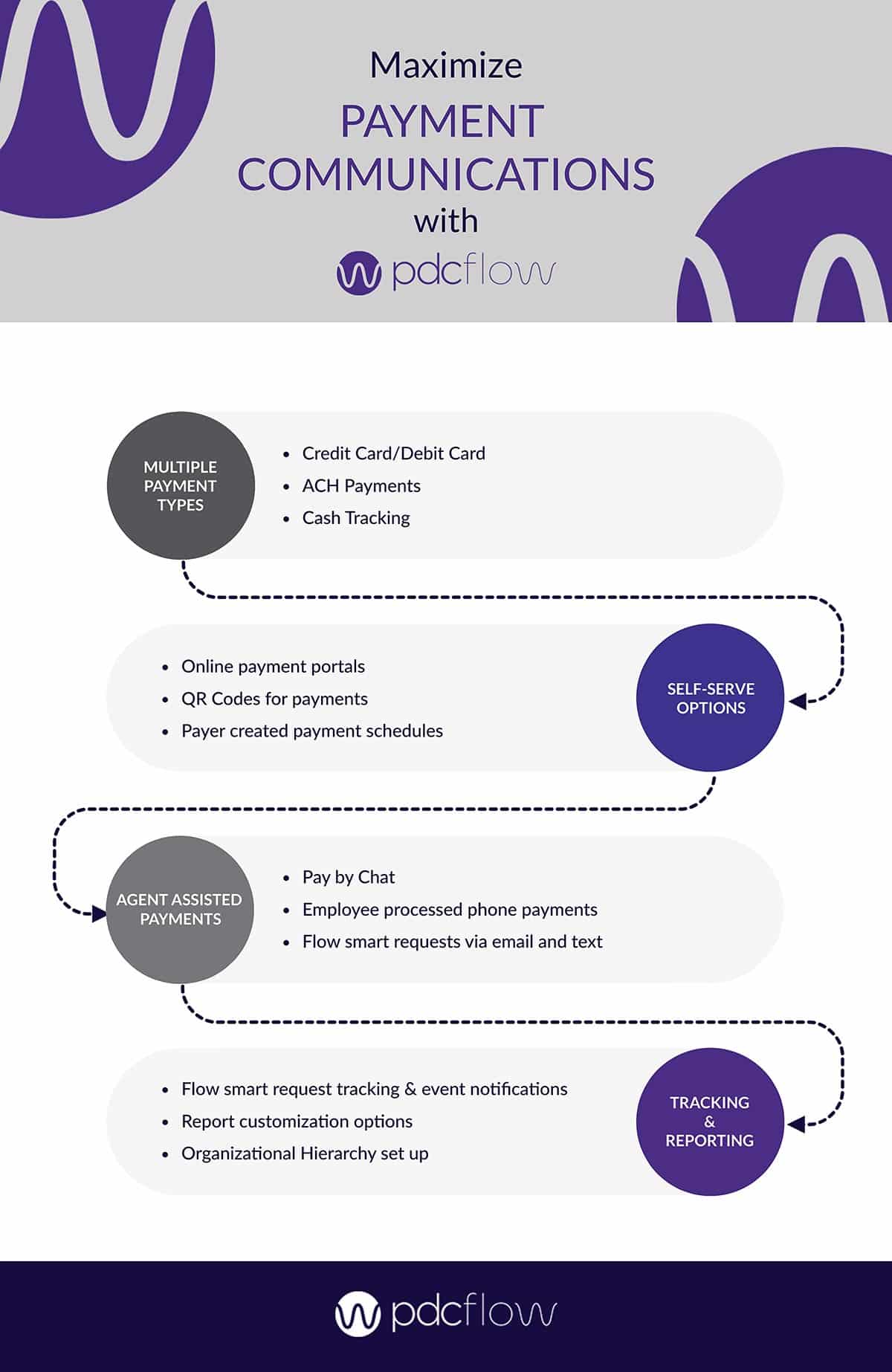

Payment Communication Software and the Payment Ecosystem

For businesses, the easier you can make your payment collection process, the smoother your business will run. When digital payments first started to become popular, most companies had to use several systems to complete their accounts receivable tasks.

As digital options gain popularity and payment processing industry trends catch up to consumer demand, companies have shifted to using fewer tools to accomplish more.

WHAT IS PAYMENT COMMUNICATION SOFTWARE?

Payment Communication Software lets you accept payment types (Credit Card, ACH and Cash) while offering modern delivery that seamlessly weaves payments workflows into your businesses digital customer journey.

Your vendor should be able to help you secure credit card and ACH processing services through merchant partnerships and offer flexible workflows and a robust reporting system to track and manage your payment communications.

Point of Sales (POS) Payments

For companies with showrooms or front desks, you may need a POS machine to take payments. When your POS technology syncs with your financial reporting system, it’s much simpler for your team. All transactions are logged in one place for reconciliation efforts.

PAYMENT COMMUNICATION FEATURES AND FUNCTIONALITY

Payment Communication Software like ours at PDCflow makes it easier to handle all of your contracts, invoices, deposits, payment authorizations—and payments from one system.

Features to look for in a payment communication system usually include:

- Email and SMS - send payment and account information to customers through the communication channels they prefer most.

- Chat compatibility - send customers directly to their unique payment form through your customer service chat or chatbot.

- Secure document delivery - digitally send contracts, invoices, statements or other sensitive documents while keeping information secure through dual authentication.

- Esignature capture - gather legally binding digital wet signatures, even when your business is 100% online.

- Photo uploads - send upload requests to customers for rentals, insurance or for a copy of photo ID.

- All-in-one workflows - combine several requests into one workflow, so customers only need a single message from your company in order to take all the actions you require.

- QR code payment links - print a QR code link to your payment portal on billing statements.

- Payment portals - offer payment portals, branded with your own logo and company colors.

- Flexible recurring payment schedules - offer flexible recurring payment schedules with term limits determined by your company and self-serve recurring payments available through your payment portal.

- Status Notifications - keep on top of progress with emailed event notifications that can let you know when messages are sent, opened and/or completed – or if a message expires or is rejected by your customer.

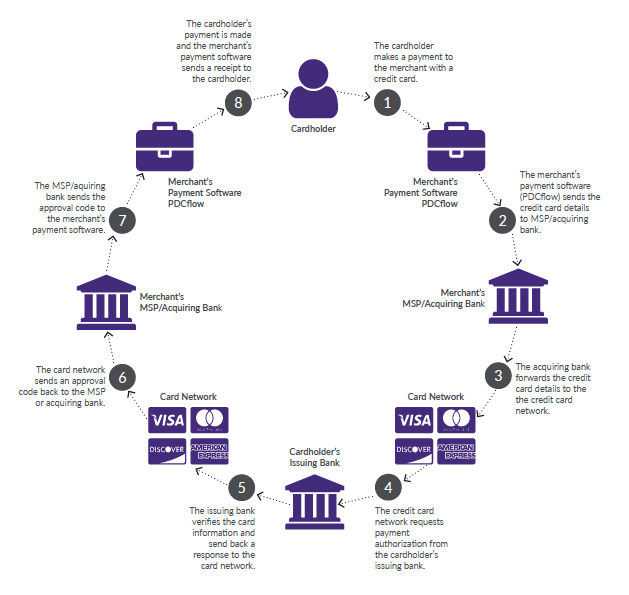

Credit Card Authorization Process

How does a credit card payment get authorized?

Credit card payments are either made in a card present transaction (where the card is used at a terminal to pay) or in a card not present transaction (where the number is given over the phone or online).

Once this happens, it can be confusing to understand where that payment data goes and how funds end up in the right place. Here is what happens next after a transaction takes place:

- The software or gateway used to make a payment sends data to the acquiring bank the merchant uses for funding. If the merchant uses a Merchant Service Provider (MSP) instead, the data is sent there.

- After the bank or MSP has what they need, the information is passed on through the credit card network. This network is a digital framework designed to pass payment information from the MSP/acquiring bank on to its next stop: the cardholder’s issuing bank.

- With the data now passed on to the cardholder’s bank, the next step is to request payment authorization. This is where the bank verifies that funds are available and all other transaction information is valid. If approved, the requested funds are put on hold and an approval, decline, or other appropriate message is sent back to the MSP/ acquiring bank through the card network.

- Back at the acquiring bank, the newly received authorization or decline is passed back to the payment software (or gateway), the payment is complete and the payment processor generates and sends a receipt to complete the transaction.

Steps in the Credit Card Authorization Process

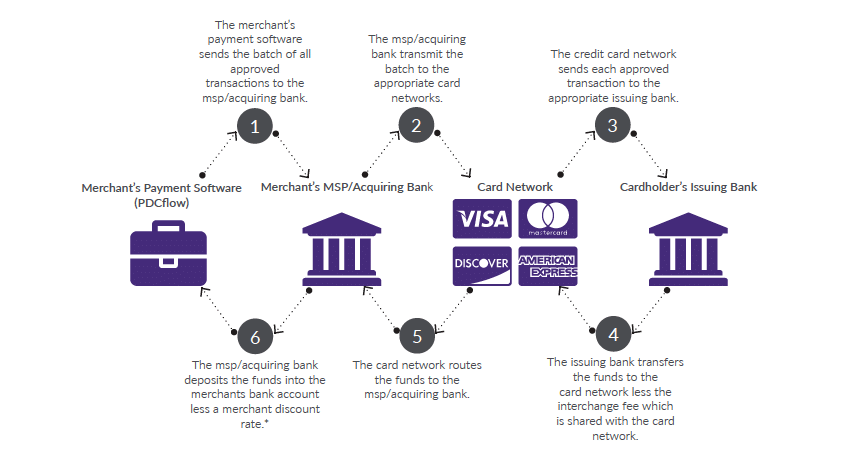

Credit Card Batching and Funding Process

WHAT IS BATCHING?

Merchants who already take credit cards should know what batching is, even if you don’t recognize the term. It is simply the process of collecting an entire group of authorized transactions and sending them to your acquiring bank or MSP all at once.

This group (batch) of already-authorized transactions is sent to your MSP/acquiring bank all at one time, usually at the end of each business day. Merchants can usually adjust when batches are sent so that reconciliation can be done in a way that fits your company’s schedule and unique business needs.

WHAT IS FUNDING?

STEPS OF BATCHING AND FUNDING

The first step is, of course, gathering all the transactions that were approved (the batch) and sending them to your MSP according to your company’s chosen batch closing time. Batching should be handled through your payment processing software or payment gateway.

Once transaction batches have arrived at the MSP or acquiring bank, the information is again passed on to the appropriate card network, such as Visa or Mastercard. Then:

- The card networks send each transaction along to the issuing bank, which then knows to debit or withdraw money from accounts and send that information back to the card network.

- The appropriate funds are transmitted back through the card network to the acquiring bank or MSP. This is where merchants are typically charged for interchange and network fees, which are subtracted from the total amount being credited.

- Finally, these funds are deposited into your merchant bank account.

Be aware, there are also MSP fees (the merchant discount or daily discount rate) that also may be taken out of the daily batch funding totals you receive or you may be charged monthly for this service (monthly discount rate).

You should get to know your vendor partners. Ask questions about the fees and billing cycles that are standard practice within their agreements so you aren’t caught off guard and don’t miscalculate your funds during reconciliation.

Credit Card Batching and Funding Process

ACH Transactions

ACH transactions (where funds are electronically transferred directly to or from a bank account) are another transaction type within the modern payment ecosystem.

Similar to the card networks that facilitate credit card payments, the Automated Clearing House (ACH) Network is governed by the National Automated Clearing House Association (NACHA). The network is a group of depository institutions that pass payment information between accounts, making ACH payments possible.

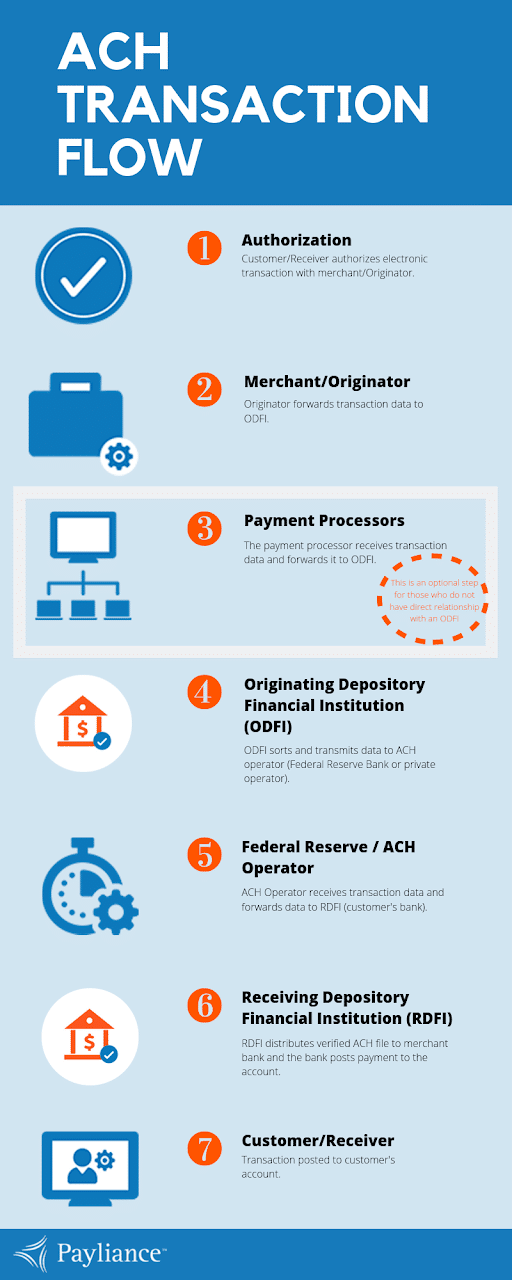

STEPS OF AN ACH PAYMENT

An ACH transaction begins when a customer agrees to make an electronic payment with your company using their bank account information. Remember to gather a payment authorization at this time to protect your business and comply with the EFTA’s Regulation E, which applies to all companies that run Electronic Funds Transfers (EFTs).

Once a customer is finished with the transaction through your front end payment processor, your software sends all the details to the Originating Depository Financial Institution (ODFI), which sorts the information and sends it along to the Federal Reserve/ACH Operator.

The reserve/operator determines where the payment information needs to go next, and delivers it to the Receiving Depository Financial Institution (RDFI). Once here, the funds are officially withdrawn from the customer’s account and deposited into your merchant account.

ACH HOLDS AND BATCHING

Payment Software Integration

For companies who want to accept credit card and ACH payments and send payment communications from their own software application, APIs are often available. Drop-in and low-code components and developer-friendly APIs can make it fast and easy to add payment functionality into your software, platform, or website.

PDCflow offers both low-code, drop-in components, and flexible, configurable APIs to best fit your customer payment communication needs.

Download Credit Card Processing and Security Guide:

Want to know more about PDCflow Software?

Press ▶️ to watch our explainer video

ONE-STEP PROCESS

- ABOUT THE AUTHOR -

Hannah Huerta, Marketing Specialist

Hannah Huerta is a Marketing Specialist at PDCflow. She creates content for the accounts receivable and payment industry.

Related Articles