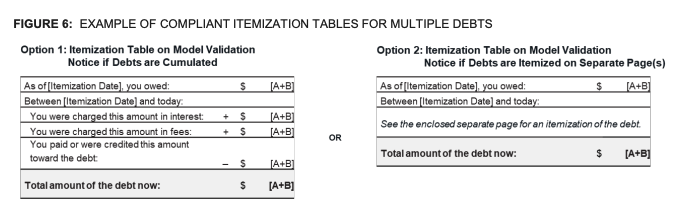

The Consumer Financial Protection Bureau issued another set of Frequently Asked Questions related to Regulation F on Friday, this time tackling the area of Validation Information and Validation Information related to Residential Mortgage Debt. The CFPB also on Friday published guidance on how collectors can use the “itemization table” in the model validation notice and offers examples of how the table might be used for different types of debts.

EDITOR’S NOTE: Leslie Bender and Joann Needleman from Clark Hill will be on an AccountsRecovery.net webinar on Tuesday, November 2 at 4:30pm ET to break down this new guidance and what it means for you with respect to complying with Regulation F. Click here to sign up for the webinar.

The questions answered by the CFPB related to Validation Information are:

- What validation information is a debt collector required to provide a consumer who owes or allegedly owes a debt?

- Is there a model validation notice in the Rule?

- Is use of the model validation notice required?

- Can a debt collector make changes to the model validation notice and still obtain a safe harbor for validation information content and format requirements?

In the guidance, the CFPB breaks down the five different itemization dates that collectors can use as part of the validation information required to be sent to consumers — the charge-off date, date of service, judgment date, transaction date, or last payment date — while also providing examples of how the itemization table might look if sending model validation notices to collect on credit card debt, residential mortgage debt, and medical debt. The guidance also tackles a problem that has been raised by many collectors, especially those collecting medical debts — how to handle situations where a collector is attempting to collect on multiple debts from the same consumer. The CFPB included examples of what itemization tables might look like for multiple debt situations, as well.