Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

You can request the removal of hard inquiries from your credit report by pointing out unauthorized checks or going through a formal dispute process with major credit agencies.

Whether you’re looking to buy a house, lease a car, or get a loan, lenders need to check your credit. To do this, they’ll perform a hard inquiry which can temporarily lower your credit score. However, if someone pulls your credit without approval, it may lead to more inquiries that can harm your credit unfairly. In cases like these, you need to know what steps to take to request the removal of inaccurate hard inquiries.

While hard inquiries are common for applying for credit, you’ll want to limit applying for new credit and avoid unauthorized inquiries as their impact stacks up fast. Learning how to navigate hard inquiries won’t just improve your financial savvy — it can also help you spot early signs of fraud or identity theft. To help you along, we’ll explain what hard inquiries are, what causes them, and the steps involved with disputing an unfair or inaccurate hard inquiry.

How To Remove Hard Inquiries from Your Credit Report

You can dispute a hard inquiry if you run into evidence of fraudulent pulls or reporting errors. By asking for the removal of these unauthorized inquiries, you protect your credit score. You can go through the dispute in seven steps:

Step 1: Review Your Credit Report

The Consumer Financial Protection Bureau recommends reviewing your credit report at least once a year to note unexpected changes. A sudden drop might indicate that unauthorized pulls impacted your credit. You should also cross reference different credit reports for discrepancies. To help, Experian®, Equifax®, and TransUnion® offer a free credit report once a year from annualcreditreport.com. Because of the pandemic, weekly for a limited time.

There are a few ways to review your credit:

- Once a year-or currently-weekly, you can order a free credit report from the largest credit bureaus: Experian, Equifax, and TransUnion. This does not include your credit score.

- Receive a free credit report card from Credit.com.

- Sign up for ExtraCredit for more in-depth credit monitoring tools.

Step 2: Note Any Inaccurate Hard Inquiries

Review the “Hard Inquiries” section of your report for signs of a credit check you didn’t authorize. If you see anything suspicious, be sure to:

- Note the furnishers or companies conducting hard inquiries you don’t recognize.

- Cross-reference those names across different reports to make sure they line up.

- Keep track of when each inquiry occurred.

- Note all inquiries you did authorize.

Step 3: Contact the Company that Performed the Inquiry

Contact the furnishers responsible for illegitimate inquiries. In some cases, these lenders will remove the reports without conducting a formal dispute. To stay prepared, make sure you:

- Get in contact with the right departments or personnel for credit report disputes.

- Share all evidence of fraud or a mistakes on the lender’s part.

- Make it clear that you want them to remove the inquiry from your report.

- If you have a past relationship with a furnisher, leverage your trust.

Step 4: Begin the Dispute Process

You can file a formal dispute if the lender doesn’t remove the inquiry from your informal request. Even if a furnisher rejects or ignores your request, you have grounds to push back. To get the ball rolling, you should:

- Review your dispute options. Some lenders use automated online systems, while others push you toward a formal dispute letter.

- Avoid handling your dispute over the phone. While this route is faster, it leaves fewer records you can use in case of legal action.

- Keep copies of every letter, email, or online submission you send regarding the dispute.

Step 5: Gather All the Necessary Information

You must include all relevant information when drafting your formal dispute letter. This may include:

- Personal information like your name, date of birth, address, and Social Security number

- The dates of all disputed inquiries and the date you sent the letter

- The entities responsible for recording the disputed hard inquiries

- The reasons why you believe agencies should remove the inquiry

- Any related documents that point to evidence of fraud or identity theft

Step 6: Submit the Dispute

With all the documentation in order, you can submit your dispute to a credit bureau. While you can contact bureaus by phone, mail, and online submissions leave a stronger paper trail.

For credit disputes by mail:

- Equifax: Equifax Information Services, LLC, P.O. Box 740256, Atlanta, GA 30374

- Experian: Experian, P.O. Box 4500, Allen, TX 75013

- TransUnion: TransUnion Consumer Solutions, P.O. Box 2000, Chester, PA, 19016

For credit disputes by online submission:

- Equifax: online dispute page

- Experian: online dispute portal

- TransUnion: online dispute page

For credit disputes by phone:

- Equifax: 886-349-5191

- Experian: 888-397-3742

- TransUnion: 800-916-8800

Step 7: Wait for the Bureau’s Verdict

Credit reporting bureaus are required to resolve your dispute within 45 days. During this time, credit agencies will contact furnishers to determine whether the credit check was fraudulent. The Fair Credit Reporting Act also holds that businesses reporting to credit bureaus must investigate disputes.

If a credit agency can’t verify the inquiry, they should remove it from your report. On the other hand, they may keep the inquiry if the furnisher insists it’s valid. If this occurs, you can:

- Pursue legal action using your past documentation as evidence.

- Look for assistance from a credit counseling company. They could help you resolve the dispute.

- Request that the bureau includes a statement on your credit report detailing the dispute. Lenders who make hard inquiries in the future will note this statement and take it into consideration.

Quick Review: What Is a Hard Inquiry on Your Credit Report?

Hard inquiries are records indicating that a furnisher reviewed your credit report as part of a credit check. Typically, lenders conduct a hard inquiry before offering you a loan or credit limit increase. Hard inquiries may drop your credit score by an average of five points. After six months to a year, the impact to credit scores will typically be less.

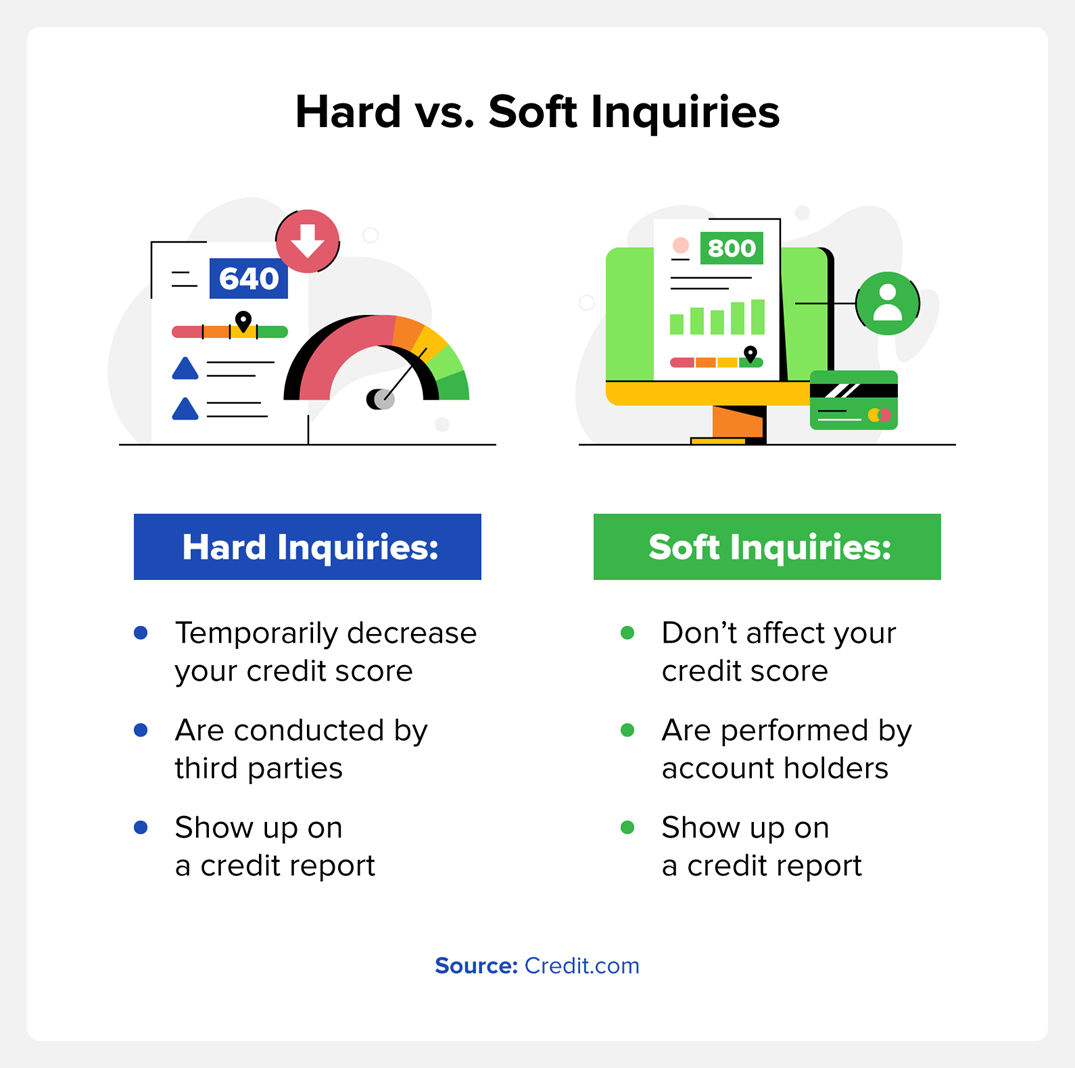

Hard vs. Soft Credit Checks

Hard and soft inquiries provide the same information about your credit. The difference lies in who ordered the credit check and why. The main differences include:

- Third parties conduct hard inquiries when they need to review your credit history. They will typically do this before issuing a loan, setting up accounts, or considering approval for housing.

- You check your own credit during a soft inquiry. A soft credit pull will not lower your credit score. You can conduct one whenever you want to review your credit. You can see your free credit score through a service like Credit.com.

Contrary to popular belief, checking your own credit score won’t lower it. That said, hard inquiries can lower your credit score. If hard inquiries occur without your consent, the Fair Credit Reporting Act allows you to remove those inquiries through a dispute.

How Hard Inquiries Affect Your Credit Score

Hard inquiries impact 10% of your FICO® credit score. However, its exact impact on the total score depends on:

- Your credit history

- Your current standing

- The time since your last inquiry

A few hard inquiries won’t lead to any long-term consequences. Additionally, the amount each hard inquiry drops your score depends on your overall financial health. Most pulls will drop the score by five points or less, but the impact goes up to 10 points. Unless a lender pulls your score multiple times by mistake, you can rest assured the credit drop will only last a few months.

How Many Hard Inquiries Are Too Many?

There isn’t a hard and fast limit to the number of hard inquiries you should request. One or two credit pulls will only drop your score by about five points each. After that point, each inquiry may lead to losses of up to 10 points.

As a general rule, don’t apply to lenders en masse. If you handle one reasonable loan application at a time, you’ll maintain a healthy score. Additionally, hard inquiries may only count against you once when shopping for home or auto loans.

How Long Do Hard Inquiries Stay on Your Credit Report

Hard inquiries stay on your credit report for around two years. However, they only affect your credit score for six months to a year. Then, two years after the inquiry, they usually age off the report.

Seven Reasons Hard Inquiries Will Show on Your Credit Report

Lenders perform hard inquiries to check your financial standing. Depending on your credit score, they may find you more trustworthy and offer loans, credit limit increases, or rentals. In general, there are seven reasons you’ll see hard inquiries on your credit report:

- Credit card applications: When applying for your first credit card at a financial institution, assume they’ll conduct a hard inquiry. When applying for a second or third card, the lender may only run a soft credit check if you’re in good standing.

- Home and auto loan applications: Lenders perform a hard inquiry before offering a large home or auto loan. However, when shopping around for favorable rates, inquiries made within 45 days of one another will only count as one inquiry.

- Rental applications: Applying to rent a home or apartment may result in a hard inquiry. While soft inquiries are more common, ask the housing manager about their approach before you apply.

- Loans: Applying for personal lines of credit or debt consolidation loans will likely involve a hard inquiry.

- Credit limit increase requests: Some financial institutions perform a hard inquiry before raising your credit limit. While most only look at your credit utilization history and conduct a soft inquiry, it’s worth asking a lender about their process.

- Reporting errors: Credit agencies can mistakenly add hard inquiries to your report. These mistakes can result from account errors, identity mismatches, or data management mistakes.

- Identity theft: Unauthorized inquiries may point toward fraud. Consult lenders with unauthorized inquiries to rule out identity theft.

FAQs about Hard Inquiries

Still have questions about hard inquiry removal and when hard inquiries fall off? We have the answers you need.

Can You Request to Have Hard Inquiries Removed?

If you applied for credit and authorized a hard inquiry from a lender, you can’t remove it from your credit report. Hard inquiries only leave your credit report if:

- Two years pass and they age off.

- The inquiry wasn’t correctly authorized, and you filed a dispute.

Does Removing Hard Inquiries Increase Your Credit Score?

Removing a hard inquiry can raise your credit score if it’s recent, but it may have no impact at all. While hard inquiries stay on your credit report for around two years, they only affect your score for about six months to a year. So, removing a hard inquiry over a year old may not raise your score.

Because of the timing, a hard inquiry falling off a credit report usually doesn’t boost the score, either. By the time an inquiry ages off, its impact on your credit score has probably passed.

How Long Does It Take to Remove a Hard Inquiry?

If you dispute an unauthorized hard inquiry, The Fair Credit Reporting Act gives furnishers and credit bureaus 45 days to investigate your dispute. However, the process can take longer, depending on your situation.

Prevent Hard Inquiries from Identity Theft and Fraud

While a few hard inquiries won’t tank your credit, they can point to financial risks. Learning the basics of cleaning your credit report and reviewing hard inquiries helps keep you aware of your credit and keep your accounts safe from fraud. While going through a dispute involves some stress, the peace of mind you get from going through the process pays for itself.

With the risk of an unauthorized inquiry, it pays to stay on top of your credit score. You can find the credit monitoring tools you need with ExtraCredit. With our service, catching errors and preventing identity theft has never been easier.

You Might Also Like

You probably know credit bureaus keep credit reports. But did you... Read More

March 7, 2023

Credit Repair

[Disclosure: Lexington Law Firm advertises on Credit.com an... Read More

March 6, 2023

Credit Repair

Your credit history and the scores based on it are important fina... Read More

May 10, 2022

Credit Repair